In the dynamic realm of real estate investment, understanding various metrics and yield measurements is crucial for gauging risks and potential returns. One such pivotal metric is the Debt Yield, which offers investors and lenders insight into the income-producing capability of an asset relative to the debt placed on it. In essence, it serves as a transparent lens through which the true risk of a loan is scrutinized, thereby playing a monumental role in decisions surrounding commercial real estate loans. This guide aims to delve deep into the intricacies of Debt Yield, exploring its definition, significance, and application in the ever-evolving real estate market.

I. Definition and Importance of Debt Yield:

a. Definition:

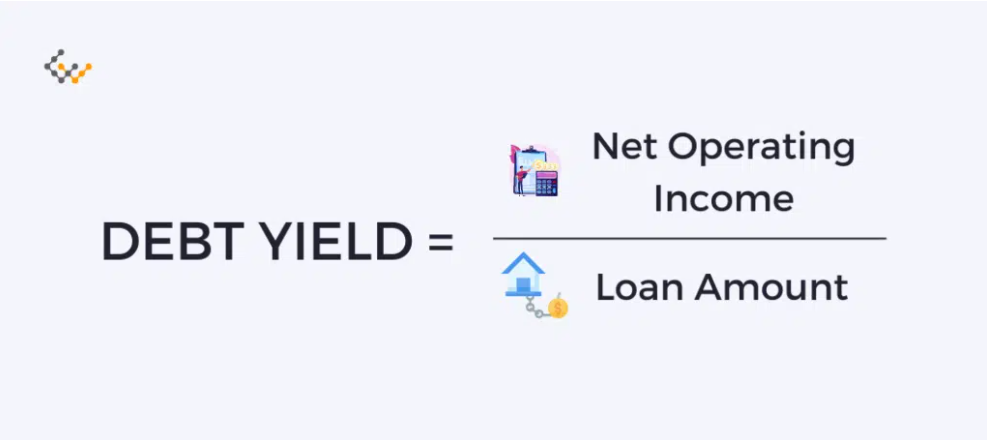

Debt Yield is a financial metric extensively used in the realm of commercial real estate to assess the level of risk associated with lending. It is calculated by dividing the property’s Net Operating Income (NOI) by the total loan amount. This ratio provides a clear and direct illustration of the annual return a lender could expect if they were to take ownership of the property, facilitating a comprehensive understanding of the financial risk inherent in lending against a specific property.

Debt Yield=Net Operating Income (NOI)Total Loan AmountDebt Yield=Total Loan AmountNet Operating Income (NOI)

b. Importance in Real Estate:

In the complex landscape of real estate, Debt Yield emerges as a paramount tool, enabling investors and lenders to analyze the income-generating potential and viability of an asset. Unlike other metrics like Loan-to-Value ratio (LTV ratio) and Debt Service Coverage Ratio (DSCR), Debt Yield is independent of capitalization rates, interest rates, and amortization schedules, offering an unbiased, clear-cut perspective of a property’s value and potential returns.

In situations where the property values and market conditions are fluctuating, Debt Yield provides a stable and reliable metric that mirrors the property’s ability to generate income, regardless of external market pressures. It acts as a beacon for lenders to traverse the turbulent seas of market variations and property value fluctuations, assisting them in making informed lending decisions.

c. Risk Assessment:

The utilization of Debt Yield as a risk assessment tool is pivotal for lenders and commercial real estate investors. A higher debt yield indicates lower risk and possibly lower leverage, as it signifies that the property’s NOI is high relative to the loan amount. Conversely, a lower debt yield represents higher risk and potentially higher leverage, denoting that the loan amount is high compared to the property’s NOI.

This clear delineation of risk enables lenders to establish minimum debt yield requirements, thus controlling the maximum loan amount extended. It acts as a protective shield, safeguarding lenders from over-leveraging and borrowers from plunging into the abyss of loan default, especially in uncertain market conditions.

d. Cap Rate vs. Debt Yield:

Cap Rate and Debt Yield are intertwined yet distinct concepts, each offering unique insights into the financial contours of real estate investments. The calculation of Cap Rate involves dividing the NOI by the property’s current market value, focusing on the rate of return on the real estate investment:

Cap Rate=NOICurrent Market ValueCap Rate=Current Market ValueNOI

Example:Consider a property with an NOI of $100,000 and a market value of $1,000,000. The Cap Rate would be 10%. If the total loan amount on the same property is also $1,000,000, the Debt Yield would also be 10%.

However, the equal Cap Rate and Debt Yield might have different investing outcomes. A 10% Cap Rate might be considered excellent in a market where average Cap Rates are lower, signifying a potential for higher returns. But a 10% Debt Yield might be perceived as risky if the lender’s minimum Debt Yield requirement is higher, reflecting a tighter income-to-debt ratio.

While Cap Rate unveils the potential profitability and market trends of a property, focusing on property values and market conditions, Debt Yield concentrates on the lender’s perspective, unraveling the true risk of a loan. Both are pivotal, serving as the twin pillars that sustain the comprehensive financial analysis, enabling investors and lenders to stride confidently in the multifaceted domain of real estate.

The formula to calculate Debt Yield is relatively straightforward:

Debt Yield=Net Operating Income (NOI)Total Loan AmountDebt Yield=Total Loan AmountNet Operating Income (NOI)

In this formula:

Net Operating Income (NOI): This represents the total income of a property after deducting all operational expenses.

Total Loan Amount: This is the total amount of the loan in question.

b. Example of Debt Yield Calculation:

Let’s consider a commercial property with an NOI of $150,000 and a requested total loan amount of $1,000,000. Utilizing the debt yield formula:

Debt Yield=$150,000$1,000,000=0.15 or 15%Debt Yield=$1,000,000$150,000=0.15 or 15%

In this scenario, the debt yield is 15%, suggesting that if a lender were to take ownership of the property, they could expect a 15% return on the investment per annum, assuming the property’s net income remains constant.

c. Implications of Debt Yield:

The implications of Debt Yield stretch far beyond a mere percentage. It essentially dictates the course of action for lenders and lays out the financial landscape for borrowers.

Good Debt Yield Example:Suppose a property has a Debt Yield of 20%. This higher Debt Yield indicates that the property’s Net Operating Income is substantial relative to the loan amount, suggesting a lower risk for lenders. In this scenario, lenders might be more inclined to approve the loan request, possibly even with favorable terms, as the likelihood of the property generating enough income to cover the loan payments is high.

Low Debt Yield Example: Conversely, a Debt Yield of 8% may raise eyebrows. This lower yield denotes higher risk, implying that the loan amount is high compared to the property’s NOI. Such a scenario might lead to stringent loan terms, higher interest rates, or even loan disapproval, as lenders might perceive the investment as precarious due to the higher leverage and lower income in proportion to debt.

Understanding the profound implications of Debt Yield is indispensable, providing a compass for lenders and borrowers in evaluating the risk and return panorama, thus enabling meticulous, informed decision-making processes in the labyrinth of commercial real estate investments.

d. Cap Rate vs. Debt Yield:

Cap Rate and Debt Yield are intertwined yet distinct concepts, each offering unique insights into the financial contours of real estate investments. The calculation of Cap Rate involves dividing the NOI by the property’s current market value, focusing on the rate of return on the real estate investment:

Calculation for Debt Yield

c. Importance of Understanding Both Yields:

Cap Rate=NOICurrent Market ValueCap Rate=Current Market ValueNOI

Example:Consider a property with an NOI of $100,000 and a market value of $1,000,000. The Cap Rate would be 10%. If the total loan amount on the same property is also $1,000,000, the Debt Yield would also be 10%.

However, the equal Cap Rate and Debt Yield might have different investing outcomes. A 10% Cap Rate might be considered excellent in a market where average Cap Rates are lower, signifying a potential for higher returns. But a 10% Debt Yield might be perceived as risky if the lender’s minimum Debt Yield requirement is higher, reflecting a tighter income-to-debt ratio.

While Cap Rate unveils the potential profitability and market trends of a property, focusing on property values and market conditions, Debt Yield concentrates on the lender’s perspective, unraveling the true risk of a loan. Both are pivotal, serving as the twin pillars that sustain the comprehensive financial analysis, enabling investors and lenders to stride confidently in the multifaceted domain of real estate.

Loan Yield refers to the total amount of interest, fees, and charges that a lender earns from a loan, expressed as a percentage of the loan amount. It provides insights into the potential income a lender can expect from a particular loan, factoring in the interest rates, loan term, and other related costs.

b. Comparison with Debt Yield:

While Loan Yield focuses on the lender’s potential income from the loan, Debt Yield concentrates on the lender’s risk associated with the total loan amount, reflecting the property’s ability to cover the debt through its income. Both metrics are crucial, but they illuminate different facets of commercial lending.

Grasping the nuances of both Loan and Debt Yield is crucial for lenders and borrowers to negotiate loan terms effectively. An understanding of Loan Yield helps in anticipating the returns, while a grasp of Debt Yield assists in assessing the inherent risks, allowing for a more balanced and informed approach to commercial real estate loans.

V. The Influence of Different Factors on Debt Yield:

a. Market Conditions:

Prevailing market conditions play a substantial role in determining Debt Yield. In environments with low-interest rates, borrowers might lean towards higher leverage, possibly leading to lower Debt Yields. Such trends can offer lucrative opportunities for property owners seeking commercial loans but can also escalate the risks associated with higher leverages and lower yields.

b. Property Type and Location:

The type and location of the property are also influential. For instance, urban development projects in areas like Los Angeles might have different Debt Yields compared to rural properties due to the variations in property values and market demands.

c. Government Agencies and Regulations:

Entities like the Federal Housing Administration and the Department of Housing play a pivotal role in shaping the landscape of commercial real estate lending. Their regulations and policies can impact Debt Yields by altering lending practices and shaping market dynamics.

VI. Conclusion:

Debt Yield stands as a pivotal metric in the realm of commercial real estate lending, acting as the beacon that guides lenders and borrowers through the intricate pathways of loan negotiations and risk assessments. It goes beyond the surface, delving deep into the financial symphony of properties, unearthing the harmonies and dissonances between income and debt.

Understanding the multi-dimensional aspects of Debt Yield, along with its counterparts like Loan Yield and Cap Rate, is paramount. It empowers stakeholders to make informed decisions, navigate market fluctuations, and realize the true potential and risks of their commercial real estate ventures.

Debt Yield will vary in different markets and Market cycles

If you want weekly insights on achieving financial independence while working your W2 subscribe!

If you would like more information about passive income ideas please contact me at jeff.davis@bridgestoneinvest.com. We have syndications going on throughout the year.

Always consult with a financial advisor, CPA, or CFP to make sure your financial plans align with your goals, risk tolerance and financial situation.

Rob Beardsley is Managing Partner of Lone Star Capital. With his team, they have acquired over $300M in Multifamily properties across Texas. I have the pleasure of knowing Rob personally, and Lone Star has given me the opportunity to partner with them on several deals in the Houston MSA which are performing according to budget.

Rob wrote his 1st book The Definitive Guide to Underwriting Multifamily Acquisitions as well as created his own Underwriting Model which he offers for free to anyone interested.

In December 2022, Rob launched his 2nd book, Structuring Debt and Raising Equity. Below is a summary of this book

The book is 2 Parts as the name suggests. Part I focuses on various debt offerings and offers details at a beginner level. He then highlights exactly how Lone Star Capital uses these existing products into deals in real time with a nuanced approach.

This flows nicely into Part II which is the larger portion of the book and directed more toward sponsors and capital raisers; however, is a good lesson for potential investors on the details they need to be aware of (that they may not be) when considering an offering.

Lone Star uses 3 keys to purchasing a Multifamily Property: buy at the right price, with the right structure and incorporate the right management. This fits well with Bridgestone Capital’s 3 Pillars of Investing: Buy Right, Finance Right and Manage Right.

This book focuses on the capital stack structure or the finance portion.

For LPs/Passive Investors understanding debt structure will allow you to create an investment criteria and determine which deals fall into this category as they come to you.

[divi_switch_layout id=”1311″]

2 Primary types of debt:

Permanent and Short-Term

Permanent (Agency)

These are 5 year terms or more and based on actual financials (T12).

Useful for no value add or small/modest value add component.

Agency debt is federally backed by Fannie/Freddie; but, originated by licensed lenders who have varying standards of underwriting.

The agency’s aim is provide liquidy to housing market and support affordable housing. Receiving quotes from various lenders is useful due to their different underwriting standards.

Short-Term

This is bridge-debt used for value-add or deep value-add properties, including those at less than 90% occupied.

Bridge debt is provided through a CLO (Collateralized Loan obligation)

It has floating rate and higher interest with varying terms among lenders

Negotiation points for Bridge Debt

Personal Guarantee

Interest reserve replenishment and Construction Completion governance

Lenders will often want signers of the loan to personally some or part of this portion of the loan

DACA (deposit Account Control Agreement )

Also known as a lockbox (this gives account control to the lender)

It is in the interest of the sponsor to keep control of the receipts and not allow the lender to get this or to mitigate this if possible.

Recourse

The recourse portion of the loan, meaning that the lender can sue the borrowers in the event of default. Some lenders will allow negotiation to partial recourse.

Interest on Unfunded Capital

The lender should not charge interest on unfunded capex. Ensure this is negotiated.

Index floor on Floating Rate Loan

Lenders want to prevent rate going under current pricing.

This is a difficult negotiating point, but possible.

Term

The longer the term, the more favorable to the sponsor.

Loan Products

Fixed & Floating

Fixed

Great terms

Eliminate interest rate risk

Prepayment penalties (Yield maintenance)

Calculated based on interest rate, prevailing risk free rate and remaining term

The higher the 10 yr treasury = lower PPP

Step down PPP is also an option: but comes with a higher interest rate

Floating rate

Research shows least interest paid when FR is used

This option is more flexible

PrePayment penalty is straightforward, typically 1% of the loan amount

Hedge on interest rate can be purchased through caps

Rate caps have increased recently due to volatility in market

The closer the cap is to market, the more expensive the cap

Part II

Structuring Debt

In order to structure the appropriate debt, first, identify property type and business plan (A,B,C,D value add). Consider leverage compared to purchase price. Items to consider:

Is capex included in the loan ?

Does leverage and term match business plan / exit strategy

Pref equity

Pref equity is a financial instrument used to build leveraged real estate capital structures. This receives priority on distributions and return of capital subordinate only to senior loan. While the senior loan offers 70-80% LTV, the pref equity can bring this up to 80-90% total, making the total capital raise only 10%.

Part III

Raising Debt

You have a property under contract, know what your business plan is, now it is time to secure a loan. You must present loan package which should contain below key elements:

Property Financials

Pro Forma / business plan

Purchase price

Capex budget

It is important to add information about the sponsorship team and track record, especially KPs (Key Principles) that will be signing on loan.

Lenders will underwrite to in place rents but proforma expenses. Therefore, it is important to make a business case of how you will lower or maintain expenses in your presentation. Having a strong story is imperative along with a strong team that was assembled well in advance.

Introduction To Equity

Two Primary Forms of Equity

Common and Preferred

Common

Does not have seniority.

Riskiest portion of the capital stack.

Sits in 1st loss position.

Benefits most on upside because unlimited profit compared to debt and pref earn fixed rate of return.

GP/LP GP ( Sponsor)

The sponsor’s role in a deal is to: find the deal, debt, equity, manage the operations and distributions. The Sponsor will incorporate fees and allocate performance compensation.

The LP role is only providing capital.

Preferred Equity

Priority over common equity

Earns fixed rate of return

Has default remedies/ control rights

Subordinate to senior loan

Mezzanine

Similar to pref

Different in legal structure

Investors hold pledge of equity as collateral

If a mezzanine borrower defaults, the mezzanine lender can obtain ownership of the pledged entity via UCC foreclosure.

These two equity options are good for low leverage value-add deals. However, having pref equity in a deal can pose a challenge to raise common equity due to increased leverage and reduced position in the capital stack.

Dual-Tranche equity structure

Puts equity into 2 groups:

Class A Pref – Fixed return

Class B Common

Class A trades upside for a more stable fixed return.

Class B can only receive cash flow after class A returns are paid.

This structure can make sense to help raise capital but not be more profitable. With this structure common equity typically receives lower cash on cash but larger overall profit.

Considerations when a deal has / needs Dual-Tranche Structure:

*Sponsor should consider: is a deal worth reducing compensation?

*Investors: is sponsor fee focused?

Elements of typical Equity Structure

Sponsor Fees

Waterfall/Promote Structure

Multi-Class Equity

The Multi-Class Equity Structure provides more than one investor tier for common equity to incentivize higher minimums from retail investors.

Class A & B

Class A – Minimum $100,000

8% Cumulative Pref

30% Promote

15% IRR (target and deal dependent)

50% Promote thereafter

Class B – Minimum $500,000

9% Cumulative Pref

Remaining distributions equal

The additional Pref for Class A is funded from GP shares, not LP; therefore there is no “loss” from investor profits for not participating in higher tier.

Sponsor Fees

Sponsor Fees are important part of compensation for sponsors

Typically, they are 1-3% of the purchase price

Also capital placement fee is 2-5% of the equity raised

This fee is less common.

Waterfalls

Waterfalls are a profit-sharing structure

The foundation is the preferred return (minimum threshold provided to LPs prior to the payment of any compensation to the sponsor

Preferred Return

Compounding – shortfalls are not simply accrued but accrued with interest at preferred interest rate

Non-compounding – No penalty for sponsor for not meeting pref return distributions

The pref may also incorporate return of invested capital meaning passive investors are entitled to pref + 100% of original investment prior to any profit-sharing with sponsor

This is additional protection to the investor

Lonestar Capital waterfall: p. 49

Refinance -> first to pref then to the capital accounts (to pay back investor principal) does not reduce ownership percentage in deal.

Some structures allow sponsor to buy out investors through refinance. In this scenario, the LP enters a deal at the highest risk point and sponsors enter at stabilization. This is not a waterfall structure. A waterfall structure puts investor capital at priority over sponsor compensation.

Promote Crystallization

Waterfall structure has downside incentives for sponsor to sell sooner. The solution is promote crystallization. In this structure, the sponsor capitalizes on value-add and receives promote before the asset is sold.

The promote to sponsor is awarded through increase in ownership percentage instead of cash which will increase cash flow, allowing the asset to be held longer.

The process includes a hypothetical sale with valuation and net proceeds run through waterfall to determine sponsor ownership.

Equity Investors

4 Types:

Retail

Co-GP

JV/Institutional

1031

1. Retail (High Net Worth Individuals)

Contribute $50-250k each. The smaller check size grants no control over major decisions. Retail Investors have a lower return hurdle than JV/Institutional

Retail Investors tend to be more capricious and will commit and back out more quickly

2. Co-GP

Capital partner that provides LP Equity by raising retail investors

This can be the most expensive way to raise capital delivering returns to LP + giving the GP compensation to Co-GP

Co-GPs are paid portion of the promote on a prorated basis

If a Co-GP delivers more than half (51%), they will want half the promote as well as their share of fees

Other value-adds can be beneficial in Co-GP model such as due diligence, Earnest Money, Lender deposit and 3rd party reports.

A Strong Co-GP can co-sign the loan satisfying lender requirements of net worth which is typically = to the loan balance.

3. JV / Institutional Capital

These partners are selective on markets and have a strict investment criteria. Institutional investors are looking to partner with someone they know, like and trust and the numbers must meet their rigorous requirements.

JV partners are very selective due to how many sponsors are vying for their capital.

In a JV, the JV Equity partner is an LP and you (sponsor) are GP.

But,the LP has major decision rights such as decision to refinance, sell and capital expenditures. LP & GP have separate classes of ownership as well as separate accounts.

IRR Hurdle

It is almost impossible for the sponsor to earn cash flow promote with an IRR hurdle. The cash flow is 1st paid to satisfy pref and surplus goes to investor principal.

*this is used @ Lone Star Capital on deals and sought on deals we will partner on at Bridgestone Capital*

4. 1031 Exchange

1031 is a major tax benefit allowing for deferral of capital gains by exchanging for like-kind property upon sale rather than receiving all sale proceeds in taxable cash.

The interest in a venture is via TIC – allows investor to exchange interest upon sale regardless of actions of other members in the venture.

The 1031 takes direct ownership and this equity type has complications to work out in process specifically with lender requirements.

Return Expectations (Metrics)

1. Cash-on-cash

Typically sought by retail investors

2-4% premium on IRR for bridge debt

Increases or decreases based on quality of asset, I/O debt vs. amortization, Hold period, loan assumption

2. YOC

Considered by Rob to be THE MOST IMPORTANT return metric

Stabilized NOI

—————————————

Purchase Price + CapEx

This is the truest form of valuation for an investment as it removes all clutter. LSC targets deals with minimum 5% but up to 7% YOC.

Raising Retail Equity

This is made up of HNWI seeking diversification from stocks or generate Cash Flow.

2 Factors influence amount of Retail Equity:

Size of your investor Universe

Degree they like and trust you

Increasing the size of the investor database is a top of funnel exercise. Creating a thought leadership platform is an effective means to build a loyal following. Offer giveaways to entice people to give their email and phone number. And, of course, being active on social media.

Continuing to offer value will increase the trust factor with your database. Offering value in the “middle of funnel” is a good practice. Setting up a phone call or additional e-books and case studies can prove useful.

Writing a book (like this one) is rare and shows you as an expert in the field and investors will associate this with trust as well.

Investor Prep

Have your company and team information ready with your story, ready to present. Also, have a set of case studies readily accessible to the investor to prove to them that you are prepared and have a track record of success.

Raising JV Equity

Rob shares that the strategies to raise institutional capital are the same as retail with consistent and value-added marketing. Sponsors should put effort into both, as institutional capital becomes more accepting.

He has had a lot of success through LINKEDIN and press releases announcing debt and Equity partners.

Rob reaches out cold with a deal under contract which creates action to underwrite and receive feedback. It is important to have a focused strategy and single-market expertise with well-organized track record. A smaller, more focused approach is better until you are proven then you can expand your markets and asset classes.

Institutional investors prefer large growth markets and assets that are 1990s build or newer. Other notable items institutional capital prefers:

Track record existent (not robust is ok)

Use case studies

Professional team

Vertical Integration is a plus

Ensures focus on the asset

Institutional grade reporting

Thorough and on-time

UW vs. Actual

Budget vs. Actual

Cash Position

CapEX Position

CapEx Budget + Operating Capital

good to include capital expenditures section outlining plan’s progress, how much has been expended and actual line-item costs

If you would like to learn more about the various types of real estate investments and syndications we have coming online, please join our investor club to gain access.

As a top-performing sales professional in supply chain/logistics for almost 20 years, Jeff Davis has been putting his commissions to work for him in real estate since 2015 and is now partnered in almost 2000 units across 4 states in the US.

In the landscape of commercial real estate investments, NNN properties stand out as a beacon of stability and predictability. These triple net lease properties offer a unique blend of long-term security and minimal landlord responsibilities, making them a magnet for both passive and active investors. As the allure of a steady income stream with low maintenance costs continues to grow, it’s essential to understand what makes these properties a solid investment and how to discern the best opportunities within this sector.

NNN properties, or triple net lease properties, are a type of commercial real estate where the tenant assumes most, if not all, of the property expenses, including real estate taxes, building insurance, and maintenance, in addition to base rent. This arrangement frees the property owner from many of the financial and operational burdens typically associated with real estate investments. In exchange, investors benefit from a reliable cash flow, often with corporate guarantees from creditworthy tenants like Dollar General, ensuring a low-risk investment that can withstand economic downturns.

The Allure of NNN Investments NNN investments are particularly attractive due to their passive nature. Investors can enjoy the fruits of their investment without the day-to-day hassles of property management. This is a good idea for those seeking to build an investment portfolio that delivers a steady income on a monthly basis without the additional expenses and time commitment involved in other types of leases, such as single net lease or double net lease properties.

Moreover, NNN properties often come with long-term leases, sometimes spanning decades, with strong tenants like fast food restaurants, convenience stores, and grocery stores. These long-term commitments provide a stable financial foundation, making NNN properties great investments with the potential for long-term appreciation and cash flow.

Navigating the Landscape:

The Importance of Location and Tenant Quality A crucial aspect of due diligence when investing in NNN properties is the assessment of property location. A prime location in a thriving local market with high traffic and visibility can enhance the value of a NNN property and ensure a solid investment. Additionally, properties occupied by tenants with a history of reliable performance, like well-known retail properties or established shopping centers, are likely to continue generating steady income, even amidst economic fluctuations.

Investing with Confidence

For those looking to delve into the world of NNN lease properties, the guidance of experienced commercial real estate investors and service providers can be invaluable. Specialists like Jeff Davis at Bridgestone Capital can help navigate the complexities of NNN lease financing and property maintenance, ensuring that investors make informed investment decisions that align with their financial goals.

Embarking on the journey of NNN property investment requires a strategic approach, a keen eye for detail, and a clear understanding of the market. With the right expertise and due diligence, investors can secure a portfolio of triple net investments that promises minimal responsibilities and a solid return on investment for years to come.

Understanding NNN Properties

The concept of NNN properties emerges as a cornerstone in the realm of commercial real estate investments, offering a unique proposition to the property owner. Also known as triple net lease properties, these investments shift the fiscal responsibilities traditionally held by landlords – such as real estate taxes, property insurance, and maintenance expenses – onto the tenants. This shift not only simplifies the investment portfolio but also enhances the attractiveness of NNN investments for those seeking long-term leases and a passive income stream.

At the core of the triple net lease’s appeal is the long-term stability it affords. Tenants in NNN lease properties are often staple commercial properties like fast food restaurants, grocery stores, and pharmacies. These businesses provide essential services that remain in demand, even during economic downturns, offering a steady income to investors. The leases are typically structured for the long term, spanning anywhere from 10 to 25 years, and are often backed by corporate guarantees, further reducing investment risk.

The lease agreement of an NNN property is a critical document, outlining the nuances of the lease term. It specifies the base rent and delineates the operating expenses that the tenant must bear, which includes everything from property taxes to insurance premiums and maintenance costs. This arrangement ensures that the investor’s involvement is limited to collecting rent and, occasionally, overseeing major structural aspects of the property maintenance.

Another advantage of NNN properties lies in their low risk profile. Unlike other types of leases such as single net lease or double net lease, the triple net lease offers an investment portfolio with minimal responsibilities for the landlord, providing a good investment opportunity for both seasoned and new commercial real estate investors. The cap rate, a critical metric used to assess the profitability of real estate investments, often reflects a lower risk in NNN investments due to the reliability of the tenant’s financial contributions.

In essence, the stability of NNN properties stems from their low-risk investment nature, the quality of tenants they attract, and the long-term leases that underpin them. Whether it’s an office building in a bustling city center or a shopping center anchored by grocery stores, the appeal of NNN properties is their ability to provide a solid investment foundation that can weather the fluctuations of the real estate market and maintain cash flow over the long time.

With these fundamental insights, investors can appreciate the unique benefits and consider how NNN properties might fit into their broader investment decisions.

The quest for the best NNN properties involves a strategic blend of market savvy and meticulous selection criteria. Identifying the cream of the crop in NNN investments goes beyond mere location; it requires an understanding of demographic trends, economic stability, and the intrinsic value of a triple net lease property.

Demographic and Economic Indicators Areas with positive population growth and robust economic indicators often present ripe opportunities for NNN property investment. A region exhibiting a steady increase in its resident count signals a blossoming economy, which in turn could translate into heightened demand for retail and service-oriented businesses. This makes such locales prime targets for NNN investments with potentially lucrative cap rates and assured cash flow.

Tenant Quality and Lease Durability

The caliber of a tenant is a defining factor in the valuation of NNN lease properties. Tenants with recession-proof businesses, such as dollar stores or grocery stores, are typically preferred. These entities tend to offer a reliable tenant base that ensures consistent rental income. Coupled with long-term leases, these tenants can offer a buffer against the volatility of economic downturns, thereby securing the investor’s net worth and maintaining the property’s status as a great investment.

Location, Location, Location

A good NNN investment also hinges on the good location of the property. Properties situated in high-traffic areas, such as shopping centers or convenience stores located at busy intersections, are more likely to attract and retain quality tenants. The property owner must also consider the local market dynamics, including the competition and the accessibility of the commercial properties.

The Role of Cap Rates The cap rate—or capitalization rate—serves as a pivotal metric in determining a good investment. It represents the potential return on an investment, assuming it’s bought in cash. A good cap rate for NNN properties is one that aligns with the investor’s risk tolerance and investment objectives. While a higher cap rate might suggest greater risk and potential return, a lower cap rate often correlates with lower risk and a more stable tenant, such as a well-known fast food restaurant chain or a retail property like Home Depot.

In sum, the best NNN tenants and properties are those that offer a confluence of advantageous demographic trends, strategic locations, and strong economic fundamentals. These factors, when combined with a solid lease agreement and a good cap rate, can yield a low-risk investment that contributes a steady passive income to the investor’s portfolio over a long-term horizon.

The attractiveness of NNN investments varies across the United States, influenced by state-specific factors such as economic growth, legal environments, and tax structures. Investors looking to capitalize on NNN lease properties must consider these regional nuances to determine which states offer the most promising opportunities.

Economic Growth and Market Health States with vibrant, growing economies often provide fertile ground for NNN properties. Investors should analyze local economic indicators like job growth, gross state product, and interest rates. States that are home to industries resistant to economic downturns, such as technology or healthcare, can be particularly appealing. Additionally, regions with a concentration of industrial parks or large shopping malls may indicate a strong demand for commercial real estate investments.

Tax Considerations and Legal Frameworks

Property taxes and state legislation can significantly impact the profitability of NNN investments. States with favorable tax laws, including lower real estate taxes and incentives for businesses, can enhance the cash flow from NNN properties. Conversely, states with complex zoning laws or high property expenses may pose additional challenges for net lease investors.

Tenant Desirability and Property Performance The best NNN tenants are often those that can leverage the demographic strengths of a state. For instance, fast food restaurants in a state with a growing population may perform better than the same brand in a stagnant or declining market. Dollar stores like Dollar General, which serve a broad customer base, can be particularly resilient tenants in states with diverse economic profiles.

Past Performance and Future PredictionsPast performance of NNN investments in a state can serve as a reliable indicator of future success. States with a track record of stable NNN property performance offer reassurance to investors. However, it’s equally important to consider future growth projections and development plans, as these can affect long-term property values and lease terms.

In conclusion, the United States offers a vast landscape of opportunities for NNN investments, but the best states for these investments are those that combine economic vitality with investor-friendly tax and legal environments. By conducting thorough due diligence and understanding the local commercial real estate market, investors can position themselves to select states that offer low-risk, high-rewardNNN properties.

Understanding the concept of a cap rate, or capitalization rate, is pivotal for investors seeking to delve into NNN properties. The cap rate is a metric used to estimate the potential return on an investment, calculated by dividing the net operating income (NOI) the property generates annually by its current market value or sale price. But the question remains: what is a good cap rate for NNN investments?

Determining a Favorable Cap Rate The definition of a good cap rate can vary depending on the investor’s strategy and the risk profile of the investment. A higher cap rate may suggest a potentially higher return but also comes with higher risk. Conversely, a lower cap rate implies less risk and a more stable investment, which is often the case with NNN lease properties. Historically, cap rates for triple net investments tend to be lower than those for more management-intensive properties, reflecting the reduced landlord responsibilities and the long-term stability of the income stream.

Market Conditions and Cap Rates Market conditions heavily influence what constitutes a good cap rate. In a high-demand, low-interest rate environment, cap rates compress, and investors might accept a lower rate due to the stability of the asset class. Conversely, in a market with higher interest rates or increased economic uncertainty, investors may expect a higher cap rate to compensate for perceived risk.

Regional Variations

Cap rates also differ geographically. NNN properties in prime locations with high commercial activity, such as office buildings in bustling city centers or retail properties in affluent suburbs, may have lower cap rates due to their desirability and lower risk. On the other hand, properties in less developed or more economically volatile areas might command higher cap rates.

Comparing Cap Rates It’s also important to compare cap rates within the same sector and local market. For example, cap rates for fast food restaurants might differ from those of grocery stores or apartment buildings. Knowing the average cap rate for similar NNN lease properties can inform whether an investment stands as a good idea or if the pricing is misaligned with the market.

In summary, while there’s no one-size-fits-all answer, a good cap rate for NNN properties is one that aligns with the investor’s goals, reflects the current market conditions, and takes into account the geographic location and type of tenant. A sound understanding of cap rates is essential in making informed investment decisions that meet long-term financial objectives.

[divi_switch_layout id=”1311″]

The Downside of Triple Net Leases

While NNN properties present numerous advantages, investors must also weigh the potential drawbacks of triple net lease agreements. Awareness of these pitfalls can aid in crafting a more resilient and informed investment strategy.

Tenant Dependency One of the core risks associated with NNN investments is tenant dependency. The property’s financial performance is closely tied to the tenant’s business success. If a tenant, even a seemingly reliable tenant like a major fast food restaurant or grocery store, fails or decides to relocate, the investor may face significant challenges in finding a new occupant, especially in specialized or less desirable locations.

Market RisksNNN lease properties are not immune to market risks. Economic downturns, shifts in consumer behavior, or changes in the local commercial real estate landscape can impact the desirability and value of a property. Moreover, interest rates and economic policies can influence investment portfolios and the overall attractiveness of NNN properties.

Long-Term Commitment

The long-term nature of NNN leases can be a double-edged sword. While it provides stability, it also means that investors have less flexibility to adjust to market changes quickly. The terms of the lease agreement may lock in a cap rate that becomes less favorable over time, especially if the market sees an increase in interest rates or a surge in property values.

Property Control The lease term typically grants tenants significant control over the property, which can lead to issues if the tenant does not adequately maintain the property or makes alterations that do not align with the owner’s interests. Additionally, at the end of a NNN lease, the property owner may inherit a property that requires substantial investment to make it leasable again.

Limited Appreciation Potential The value of NNN properties is largely derived from the income they generate rather than the potential for property appreciation. While this can lead to a steady cash flow, it may also result in lower overall returns compared to other real estate investments that offer both income and appreciation potential.

Financing Challenges

Financing for NNN investments can also pose challenges. Lenders may enforce stricter loan-to-value ratios or higher interest rates due to the perceived risks associated with single-tenant properties. Furthermore, the net lease investors need to consider the impact of financing costs on their overall returns, especially if they are relying on NNN lease financing to complete the purchase.

In summary, while NNN properties can be a solid investment with minimal responsibilities for the landlord, it’s crucial to perform comprehensive due diligence and consider the long-term implications of a triple net lease. Understanding these potential downsides can help investors make more informed decisions and develop strategies to mitigate risks associated with triple net investments.

Spotlight on Ideal NNN Tenants

Identifying the best NNN tenants is critical for ensuring the success of NNN investments. Ideal tenants are those who provide a steady income through reliable business operations and have the financial strength to withstand economic downturns. Here are key attributes that characterize the most sought-after tenants in NNN lease properties.

The financial stability of a tenant is paramount. Tenants with strong credit ratings and a history of solid investment performance provide assurance of long-term lease commitments. A corporate guarantee from a reputable company, such as Dollar General or Home Depot, further strengthens the tenant’s reliability by backing the lease with the corporation’s assets.

Recession-Resistant Operations Tenants operating in recession-resistant industries, such as grocery stores, pharmacies, and essential service providers, are particularly desirable. These businesses tend to maintain consistent operations regardless of the economic climate, ensuring a continuous cash flow for investors.

Longevity and Track Record

Tenants with a long-standing presence in the market and a track record of past performance are more likely to continue their success in the future. This is especially true for well-known retail properties and fast food restaurants that have weathered various market cycles.

Alignment with Market Trends The best tenants are those whose business models align with current and emerging market trends. For example, convenience stores and medical facilities have seen growing demand due to changing consumer preferences and demographic shifts.

Lease Structure and Terms An ideal NNN tenant agrees to favorable lease terms that protect the interests of the property owner. This includes taking responsibility for most, if not all, property expenses, including real estate taxes, insurance premiums, and maintenance costs. The type of lease should reflect a clear understanding of responsibilities, ensuring the property owner has minimal responsibilities.

In essence, the best NNN tenants are those who offer financial stability, operate in resilient industries, have a strong market presence, and agree to lease terms that safeguard the investor’s returns. By securing tenants that tick these boxes, investors can ensure their NNN properties remain a low-risk investment with a potential for long-term investments and a stable return on their investment portfolio.

Financial Aspects of NNN Investments

The allure of NNN investments lies not only in their structural simplicity but also in the financial predictability they offer to investors. Several key financial aspects define the attractiveness of these investments.

Base Rent and Incremental Increases The base rent is the foundational income from a NNN property, usually established as a fixed amount or tied to a formula that includes periodic increases. These incremental rent hikes are often tied to the Consumer Price Index (CPI) or a predetermined percentage, contributing to a steady income growth over the lease term and countering inflationary pressures.

Understanding Operating Expenses In NNN lease properties, tenants typically bear most, if not all, operating expenses. This includes real estate taxes, insurance premiums, and maintenance costs. For the investor, this means the cash flow from the base rent is not diluted by these expenses of the property, making it a more net lease investment.

Property Taxes

Property taxes can be a significant expenditure in commercial real estate investments. In the NNN model, tenants are responsible for these taxes, alleviating the investor from variable costs that can fluctuate with local government assessments and rate changes.

Insurance and Maintenance Tenants in NNN investments typically cover building insurance and property maintenance costs. This not only reduces the additional expenses for the owner but also motivates tenants to maintain the property well, potentially preserving the property’s value over time.

The Triple Net Lease Advantage The financial structure of the triple net lease ensures that the property owner is largely insulated from the financial vagaries of property management. While gross leases require landlords to pay for various property-related costs, NNN properties provide a more hands-off approach, allowing for a more passive income stream.

Cap Rate Considerations

The cap rate remains a critical measure for evaluating the potential return on an NNN property. A good cap rate reflects a balance between risk and reward, with NNN properties typically offering lower rates due to their stability and long-term investment appeal.

Financing NNN Investments While NNN properties are attractive, they also require substantial capital outlay. NNN lease financing can be a strategic tool for investors, allowing them to leverage their capital while securing a potentially lucrative asset. However, investors must carefully consider loan terms and interest rates to ensure that financing costs do not erode the benefits of their investment portfolio.

In conclusion, the financial aspects of NNN properties—from base rent to operating expenses—are designed to favor the investor, providing a clear and predictable income stream. By meticulously assessing these financial elements, investors can reinforce their portfolios with investments that promise both stability and profitability.

NNN Investment Strategies

Developing a robust NNN investment strategy is essential for maximizing returns while minimizing risks. Investors must navigate various elements, from due diligence to selecting the right mix of properties, to ensure that their foray into NNN lease properties is successful.

Strategic Acquisition Selecting the right NNN property requires thorough due diligence. This includes evaluating the tenant’s business health, the property’s physical condition, and the lease’s legal stipulations. The goal is to secure low-risk investments that offer steady income and align with the investor’s long-term investment goals.

Portfolio Diversification

Diversifying across different types of NNN properties, such as office buildings, retail properties, and fast food restaurants, can spread risk. Investing in a mix of geographies and tenant business types can protect the portfolio against localized economic downturns and industry-specific downturns.

Understanding Lease Terms The lease term and structure are fundamental to NNN investments. Investors should seek lease agreements that place most of the financial and operational responsibilities on the tenant, including property taxes, insurance premiums, and maintenance expenses. A long-term lease with a reliable tenant provides a predictable cash flow.

Exit Strategy Planning

Even though NNN properties are generally long-term investments, having a clear exit strategy is crucial. This could involve selling the property at a point where the cap rate is favorable or when market conditions predict a significant appreciation in value. NNN investors should also consider the implications of lease durations and tenant renewals on the property’s salability.

Utilizing Professional Expertise Leveraging the knowledge of experienced brokers and advisors who specialize in NNN lease financing and investments can be invaluable. These professionals can offer insights into the best ways to structure deals, identify promising properties, and navigate the intricacies of the commercial real estate market.

Tax Considerations

Investors should also consider the tax implications of NNN properties, including real estate taxes and the potential benefits of cost segregation. Consulting with tax professionals can help investors optimize their tax situation, which can enhance the overall return on investment.

In summary, a successful NNN investment strategy involves careful selection of properties, strategic diversification, in-depth understanding of lease terms, forward-thinking exit planning, and the utilization of professional expertise. By following these strategic guidelines, investors can build a resilient and profitable NNN investment portfolio.

Leveraging Professional Expertise

The complexities of NNN investments necessitate the expertise of seasoned professionals who can navigate the intricacies of the market and provide strategic insights. Professional advisors, including brokers, financiers, and legal experts, play an integral role in guiding investors toward making informed decisions.

Broker Expertise

NNN brokers specialize in identifying and evaluating potential NNN properties. They have a deep understanding of market trends, cap rates, and tenant strengths. An experienced broker can provide invaluable guidance on selecting the best NNN tenants and negotiating favorable lease terms that align with an investor’s financial goals.

Financing Guidance

Financing is a critical component of commercial real estate investments. Financial advisors and mortgage brokers can help investors understand the nuances of NNN lease financing, from assessing loan-to-value ratios to navigating the interest rates and loan covenants. This expertise is crucial in ensuring that the financing structure supports the investment’s profitability and long-term sustainability.

Legal and Tax Counseling Engaging legal professionals is important for reviewing and structuring lease agreements to ensure they protect the investor’s interests. Legal experts can also assist with due diligence, ensuring compliance with all local laws and regulations. Tax professionals, on the other hand, can advise on structuring the investment to maximize tax benefits, such as 1031 exchanges for deferring capital gains taxes.

Property Management and Maintenance While NNN properties are generally low maintenance, some level of oversight is still necessary. Property management companies can oversee the day-to-day operations and ensure that tenants adhere to the lease agreement, including maintaining property expenses and insurance premiums.

Partnering with Professionals

For investors looking to enter or expand their presence in the NNN market, partnering with professionals like Jeff Davis at Bridgestone Capital can provide a competitive edge. These experts can facilitate access to off-market deals, provide insights into emerging trends, and help investors build a diversified investment portfolio.

Call to Action

If you’re considering NNN investments as a means to secure a passive income stream or to diversify your investment holdings, reaching out to a knowledgeable advisor is a prudent first step. Contact Jeff Davis at jeff.davis@bridgestoneinvest.com to explore our list of deals open only to those in our exclusive deal club..

In conclusion, tapping into the expertise of professionals can significantly enhance an investor’s ability to navigate the NNN property market effectively. This expertise can lead to better investment decisions, optimized financial structuring, and ultimately, a more profitable and low-risk investment experience.

Conclusion

Navigating the world of NNN properties requires a blend of market knowledge, strategic planning, and a keen eye for detail. These investments offer the allure of passive income and long-term leases, which can make them an attractive component of a diversified investment portfolio. However, success in this arena isn’t simply a matter of choosing the right property; it involves a comprehensive approach that includes due diligence, understanding the nuances of lease agreements, and recognizing the importance of tenant quality.

As investors consider adding NNN lease properties to their portfolios, they must weigh the low-risk investment potential against the responsibilities and possible downsides. While NNN investments can provide steady income and minimal responsibilities for the landlord, they also demand attention to changing market conditions, tenant solvency, and the impacts of economic cycles.

In this journey, the guidance of seasoned professionals is invaluable. From navigating NNN lease financing to ensuring that property taxes and maintenance expenses are adequately covered by the tenant, experts can help tailor an investment strategy to an individual’s goals and risk tolerance. They can provide insight into the best practices for property management, help interpret cap rate fluctuations, and assist with investment decisions.

For those ready to explore the stable yet dynamic sector of NNN investments, now is the time to act. With the right approach, these properties can be a source of solid investment returns and a low-risk path to achieving financial goals. By staying informed, leveraging professional advice, and staying attuned to market shifts, investors can confidently step into the realm of NNN properties and secure their financial future.

Interested in exploring NNN investment opportunities?

Reach out to Jeff Davis at Bridgestone Capital via jeff.davis@bridgestoneinvest.com for expert advice and start building a real estate portfolio that stands the test of time.

Gain insights on achieving financial independence while working your W2 subscribe!

To receive information about passive income ideas please contact me at jeff.davis@bridgestoneinvest.com. We have syndications going on throughout the year.

Always consult with a financial advisor, CPA, or CFP to make sure your financial plans align with your goals, risk tolerance and financial situation.

RSS Error: WP HTTP Error: A valid URL was not provided.

In the intricate realm of personal finance, few debates resonate as profoundly as the clash between 401(k) plans and real estate investments. The stakes are high, with each contender vying for supremacy in the realm of retirement planning and financial freedom. This contentious discourse has given rise to impassioned proponents and fervent detractors on both sides.

Understanding the weightiness of this decision is paramount, as it shapes the trajectory of your retirement and financial independence. In this critical analysis, we delve into the advantages and drawbacks of both options, equipping you with the insights needed to navigate this pivotal juncture in your financial journey.

Register for our insightful masterclass webinar on the 12 Steps to Financial Freedom for Physicians!

401(k) vs. Real Estate: A Comprehensive Comparison

Let’s embark on a journey to dissect and compare the nuances of investing in your 401(k) against the allure of real estate. To lend clarity to this multifaceted dilemma, we’ll unravel the intricacies of each, providing you with a roadmap to decide which path aligns seamlessly with your financial aspirations.

Investing in your 401(k) encompasses a broader scope, encapsulating various tax-advantaged traditional retirement accounts such as 401(k)s, 403(b)s, 457(b)s, or Individual Retirement Accounts (IRAs). The nomenclature is inconsequential; what matters is the act of strategically placing your funds into a tax-advantaged space for investment purposes.

Simplify your investment journey by automating 401(k) contributions.

Establish a savings rate (ideally ≥ 20% of gross income) and effortlessly channel funds into your tax-advantaged account.

Opt for low-cost, diversified index mutual funds to streamline your investment strategy.

Tax Advantages:

Benefit from the pre-tax nature of 401(k) contributions, fostering tax savings in the present.

Experience tax-free growth within the 401(k) until withdrawal in retirement, optimizing long-term returns.

Mitigate current taxable income, strategically positioning your financial portfolio.

Security and Protection:

Safeguard your assets from potential liabilities through the inherent protection of 401(k) and tax-advantaged accounts.

Alleviate concerns about exposure to legal risks, enhancing the safety of your retirement savings.

Employer Match:

Leverage the significant advantage of employer-matched contributions, a form of free money that enhances your overall investment portfolio.

Seize the opportunity to maximize employer contributions, an invaluable asset in your pursuit of financial growth.

Safety with Responsible Management:

Navigate the market with prudence by adopting a responsible investment approach.

Opt for low-cost, diversified index funds to capitalize on the inherent stability of 401(k) plans.

Embrace passive investing, a strategy that has historically outperformed active management.

With these advantages in mind, we lay the groundwork for a comprehensive exploration of the intricate facets of 401(k) plans and real estate investments. The journey ahead entails unraveling the distinctive strengths of each and discerning which resonates more profoundly with your unique financial goals.

Stay tuned for the next installment as we delve into the unparalleled allure of real estate investments and how they stack up against the formidable 401(k) contender.

The Unrivaled Allure of Real Estate Investments: A Rivalry with 401(k) Plans

As the spotlight now turns to real estate investments, we unravel the distinctive advantages that set this contender apart in the grand debate against 401(k) plans. Real estate stands as a formidable rival, offering a different set of potentials and benefits that appeal to a diverse array of investors.

Advantages of Real Estate Investments vs. 401(k) Plans

Potential for Higher Returns:

Real estate investments often boast higher returns compared to the potentially volatile nature of the stock market within 401(k) plans.

Strategic investment in cash-flowing real estate, with a focus on expected cash-on-cash returns of 10% or greater, can unlock substantial financial gains.

Diverse Revenue Streams:

Beyond cash flow, real estate provides various avenues for generating income.

Benefit from equity build-up through rental income, forced appreciation by optimizing property finances, and protection against inflation, ensuring a diversified income portfolio.

Robust Tax Advantages:

Enjoy substantial tax benefits within the realm of real estate investments.

Leverage property depreciation to create passive paper losses that offset passive income from rental cash flow.

Explore accelerated bonus depreciation options and potential real estate professional status for enhanced tax advantages.

Asset Protection:

Shield your investments through meticulous asset protection structures, such as establishing Limited Liability Companies (LLCs).

Create a distinct entity, safeguarding your personal finances from potential risks associated with your real estate ventures.

Leverage as a Wealth Accelerator:

Embrace the unparalleled advantage of leveraging borrowed funds to purchase real estate.

Multiply your investment potential by using a mortgage for property acquisition, allowing you to benefit from 100% of the property’s value while only investing a fraction.

Limitless Investment Potential:

Unlike the capped contribution limits of 401(k) plans, real estate investments offer limitless potential.

Ideal for those with a robust appetite for retirement savings, real estate allows for flexible investment amounts tailored to individual financial goals.

Flexibility with Withdrawals:

Escape the constraints of early withdrawal penalties prevalent in 401(k) plans.

Real estate investments provide the freedom to utilize funds as needed, offering unparalleled flexibility outside the rigid confines of retirement age requirements.

Navigating Market Inefficiencies:

Seize opportunities presented by the inefficiencies of real estate markets, especially in smaller, less efficient local markets.

Capitalize on market inefficiencies for strategic investments, fostering growth and wealth creation.

Real estate emerges as a compelling alternative, showcasing a myriad of benefits that align with diverse financial goals. Stay engaged as we navigate the nuanced landscape of real estate vs. 401(k), drawing closer to a comprehensive understanding of these two financial powerhouses.

Who Wins?

Finding Harmony in Divergence – Coalescing 401(k) and Real Estate for Optimal Wealth

As the debate unfolds, we arrive at a pivotal crossroads where the clash between 401(k) plans and real estate investments transforms into a synergistic approach. The question arises: must one choose between these financial titans, or can a harmonious coexistence amplify the path to financial freedom?

Navigating the Intersection: Integrating 401(k) and Real Estate Strategies

The good news emerges on this financial battleground: the conflict need not end with a clear victor. Investors possess the liberty to embrace both realms, orchestrating a strategic blend that leverages the strengths of 401(k) plans and the allure of real estate. Here, we unravel the possibilities and advantages of a hybrid investment strategy.

Maximizing Tax-Advantaged Accounts:

Initiate your financial journey by maximizing contributions to tax-advantaged accounts, including 401(k) plans.

Optimize employer matches and capitalize on the tax advantages bestowed by these retirement vehicles.

Real Estate as a Cash-Flowing Companion:

Allocate surplus funds beyond tax-advantaged accounts into real estate investments.

Cultivate a robust portfolio with a focus on cash-flowing properties, ensuring a steady stream of income.

Unlocking the Potential of Self-Directed IRAs:

Explore the avenue of self-directed Individual Retirement Accounts (IRAs) for expanded investment horizons.

Navigate beyond traditional stocks and bonds, venturing into real estate and other alternative assets for diversification.

Harnessing Self-Directed IRAs for Real Estate:

Delve into the potential of self-directed IRAs for real estate investments, broadening your retirement portfolio.

Navigate the intricacies of rules and restrictions, ensuring compliance while tapping into the benefits of real estate diversification.

Real Estate Syndications for Collective Power:

Consider real estate syndications as a collaborative investment approach.

Pool resources with fellow investors, accessing larger and potentially more lucrative real estate opportunities.

Utilizing 401(k) for Real Estate Ventures:

Explore the option of using a 401(k) for real estate investments, expanding the scope of your retirement portfolio.

Delve into the rules, risks, and rewards associated with using retirement funds for real estate ventures.

Strategic Allocation Based on Financial Goals:

Tailor your investment strategy based on individual financial goals, risk tolerance, and timeline for returns.

Recognize the flexibility of a hybrid approach, allowing for a personalized blend that aligns seamlessly with your aspirations.

In the intricate dance between 401(k) plans and real estate, a hybrid strategy emerges as a beacon of financial ingenuity. The ability to maximize tax advantages while venturing into the robust realm of real estate investments unlocks a world of possibilities. Stay engaged as we delve deeper into the nuances of this hybrid approach, offering insights into the seamless integration of these two financial powerhouses.

The Intersection of Tax Benefits: Real Estate and Retirement Harmony

As we navigate the labyrinth of financial choices, the synergy between real estate and retirement plans becomes increasingly evident. In this section, we delve into the intersection of tax benefits, shedding light on how real estate investments and retirement plans can harmoniously coexist, offering a wealth of advantages to savvy investors.

Maximizing Tax Breaks Through Real Estate:

Real estate investments open doors to substantial tax advantages.

Dive into the world of deductions, leveraging breaks on mortgage interest, property taxes, and various expenses to optimize your tax position.

Individual Retirement Account (IRA) Flexibility:

Unleash the potential of traditional and Roth IRAs in crafting a tax-efficient retirement strategy.

Explore the tax-deferred growth of traditional IRAs and the tax-free withdrawals in retirement offered by Roth IRAs.

Real Estate Investment Trusts (REITs):

Consider the benefits of Real Estate Investment Trusts (REITs) within your investment portfolio.

Delve into the tax advantages and potentially higher returns associated with including REITs in your retirement and investment strategy.

Navigating Capital Gains in Real Estate:

Capitalize on the potential for capital gains in the real estate market.

Understand how strategic investment decisions can lead to substantial returns and navigate the tax implications of capital gains.

The Role of Family Members in Real Estate Ventures:

Explore the option of involving family members in real estate investments.

Recognize the potential for collaborative ventures that align with both investment goals and family wealth building.

Real Estate Business Dynamics:

Unravel the intricacies of real estate as a business, emphasizing the importance of sound financial practices.

Leverage the tax benefits and financial flexibility offered by a well-structured real estate business.

Unlocking the Power of Long-Term Investments:

Embrace the concept of real estate as a long-term investment strategy.

Harness the potential for sustained growth and wealth accumulation through a well-managed portfolio of real estate assets.

Creative Approaches to Retirement Assets:

Innovate in the realm of retirement planning, exploring creative approaches to diversify your assets.

Consider the integration of real estate, precious metals, and alternative investments to craft a robust and resilient retirement portfolio.

Balancing Real Estate and Retirement Goals:

Strike a balance between real estate endeavors and retirement aspirations.

Tailor your investment strategy to align with both short-term cash flow objectives and long-term retirement goals.

As we navigate the intricate landscape of tax benefits, the amalgamation of real estate investments and retirement plans emerges as a strategic powerhouse. Stay tuned as we unravel more layers, offering insights into the seamless fusion of these financial elements for optimal wealth creation.

For access to our commercial real estate deal flow and passive income ideas, connect with Bridgestone Capital at jeff.davis@bridgestoneinvest.com or join our newsletter here.

Harnessing the Potential – Real Estate in Retirement Accounts

In this segment, we explore the intricacies of integrating real estate into retirement accounts, unraveling the potential benefits and considerations of this strategic move.

Self-Directed IRA Advantages:

Delve into the realm of self-directed IRAs and their role in empowering investors with broader choices.

Uncover the flexibility to invest in real estate within the framework of a self-directed IRA, expanding your investment horizons.

Strategic Use of Roth IRA:

Explore the strategic use of Roth IRAs in the context of real estate investing.

Understand how Roth IRAs can offer tax-free growth and withdrawals, enhancing the appeal of real estate within a retirement account.

Navigating the Real Estate Syndication Landscape:

Navigate the landscape of real estate syndications within retirement accounts.

Grasp the benefits of pooling resources through syndications, unlocking access to larger and potentially more lucrative real estate investment opportunities.

Cautionary Considerations:

Delve into the cautionary considerations of real estate investments within retirement accounts.

Understand the rules and restrictions, such as limitations on personal use of the property, to ensure compliance with self-directed IRA regulations.

Weighing the Pros and Cons:

Evaluate the pros and cons of utilizing retirement accounts for real estate investments.

Weigh the potential benefits, such as portfolio diversification, against the regulatory constraints and risks associated with this approach.

Real Estate Professional Status (REPS):

Uncover the potential for achieving Real Estate Professional Status (REPS) and its impact on tax benefits.

Explore the eligibility criteria and the strategic use of REPS to offset active W2 or 1099 income with paper real estate losses.

Real Estate Investment Trusts (REITs) in Retirement Accounts:

Assess the role of Real Estate Investment Trusts (REITs) within retirement accounts.

Understand how REITs can provide exposure to real estate assets without the direct management responsibilities.

Building Wealth with Real Estate in Retirement:

Gain insights into building wealth through real estate investments in retirement.

Leverage the unique advantages of real estate, such as cash flow, tax benefits, and potential appreciation, to create a robust retirement portfolio.

As we journey deeper into the fusion of real estate and retirement accounts, the landscape of possibilities expands. Stay engaged as we unravel more layers, providing a comprehensive guide to navigating the intersection of real estate and retirement planning.

To learn more about how we get outsized returns on real estate passively, learn more by contacting us: at jeff.davis@bridgestoneinvest.com or subscribe to our newsletter here.

Navigating the Crossroads – Real Estate vs. Traditional Investments

Now, let’s delve into the critical decision-making process when faced with the choice between real estate and traditional investments, addressing key considerations and factors.

Risk Tolerance and Investment Goals:

Assess your risk tolerance and investment goals to determine the most suitable path.

Recognize that individual preferences, financial aspirations, and risk appetite play a pivotal role in shaping your investment strategy.

Market Dynamics and Investment Landscape:

Explore the dynamics of both the real estate and traditional investment markets.

Understand the potential risks and rewards associated with each option, considering factors like market volatility, historical performance, and economic trends.

Tax Implications and Strategies:

Examine the tax implications of real estate investments compared to traditional investment vehicles.

Evaluate the tax advantages and disadvantages, including considerations like capital gains, deductions, and the impact on overall taxable income.

Diversification Strategies:

Uncover the role of diversification in building a resilient investment portfolio.

Consider how real estate and traditional investments contribute to diversification, mitigating risks and enhancing the overall stability of your financial portfolio.

Leverage and Financing Opportunities:

Delve into the leveraging opportunities offered by real estate investments.

Understand how leveraging can amplify returns and provide access to larger investment opportunities, distinguishing real estate from traditional investment avenues.

Flexibility and Liquidity:

Evaluate the flexibility and liquidity aspects of both real estate and traditional investments.

Recognize that real estate investments may offer less liquidity but can provide stability and consistent cash flow, while traditional investments may offer more liquidity but with potential market volatility.

Long-Term vs. Short-Term Perspectives:

Consider the time horizon of your investment strategy.

Recognize that real estate investments often align with long-term wealth accumulation, while traditional investments may cater to those seeking shorter-term gains.

Consulting Financial Advisors:

Emphasize the importance of seeking advice from financial professionals.

Engage with financial advisors to align your investment choices with your financial goals, risk tolerance, and overall wealth-building strategy.

By navigating these considerations thoughtfully, investors can make informed decisions tailored to their unique circumstances. Whether it’s the stability of real estate or the liquidity of traditional investments, the key lies in aligning your choices with your financial objectives.

To learn more about how we get outsized returns on real estate passively, learn more by contacting us: at jeff.davis@bridgestoneinvest.com or subscribe to our newsletter here.

Unleashing the Power of Self-Directed IRAs in Real Estate Investment

Now, let’s unravel the potential of self-directed IRAs as a dynamic tool for real estate investment. Delving into the intricacies, benefits, and strategies involved can open new avenues for investors seeking alternative routes to financial freedom.

Understanding Self-Directed IRAs:

Explore the concept of self-directed IRAs as a versatile retirement savings vehicle.

Differentiate self-directed IRAs from traditional IRAs, recognizing the broader range of investment options they offer, including real estate.

Diversification through Real Estate:

Highlight the role of real estate in diversifying self-directed IRA portfolios.

Emphasize the potential benefits of incorporating real estate assets, such as rental properties or real estate investment trusts, into a self-directed IRA for enhanced portfolio resilience.

Tax Advantages and Considerations:

Illuminate the tax advantages associated with real estate investments within self-directed IRAs.

Examine potential deductions, tax-deferred growth, and other advantages that contribute to a tax-efficient wealth-building strategy.

Navigating Rules and Restrictions:

Navigate the specific rules and restrictions governing real estate investments within self-directed IRAs.

Address considerations like prohibited transactions, disqualified persons, and essential guidelines for compliance.

Powerful Tools for Wealth Accumulation:

Showcase self-directed IRAs as powerful tools for accumulating wealth beyond traditional investment avenues.

Discuss how investors can leverage self-directed IRAs to explore diverse assets, including precious metals, private placements, and real estate.

Real Estate Syndications within Self-Directed IRAs:

Introduce the concept of real estate syndications as a collaborative investment strategy within self-directed IRAs.