Estimated reading time: 9 minutes

Table of contents

The allure of tax benefits often draws investors toward becoming a Limited Partner (LP) in real estate syndications. It is the allure of passive income reduced by tax deductions. An investor must know the documentation and process to know what to expect. Otherwise, the schedule K-1 tax forms could be daunting. Deconstructing this document will prove beneficial for all the K-1s you will receive in syndications.

These tax perks are channeled through the Schedule K-1 tax form (Form 1065), an IRS document that holds significance for Passive Investors.

This form is pivotal for any individual in a business partnership agreement, as it must be filed with the IRS. The K-1 sheds light on the past fiscal year’s earnings, losses, and sharing dynamics among individual partners.

My initial encounter with the Schedule K-1 form was quite bewildering, and many of our newest Supply Chain Investor Club members have shared similar sentiments.

This article aims to deconstuct the complexities and provide a comprehensive understanding of the IRS Schedule K-1 tax form, especially concerning your annual tax return for passive investors.

*This information is provided for educational purposes only and does not constitute tax advice. Please consult with a tax professional or preparer for personalized advice regarding your tax situation.

If you want weekly insights on achieving financial independence while working your W2 subscribe!

What is Equity Multiple in Commercial Real Estate(Opens in a new browser tab)

[divi_switch_layout id=”1311″]

Exploring the Schedule K-1 Tax Form

The Schedule K-1 tax form is a federal document that outlines the income you’ve earned (or lost) and any dividends you’ve received from your involvement in a private investment such as a:

- Limited Partnership (LLP)

- Limited Liability Corporation (LLC)

- S Corporations

You can access the K-1 on the IRS.gov website. Click HERE.

Investors in pass-through entities do not pay tax at the partnership level. Instead, they pay taxes directly to the Internal Revenue Service (IRS) via your tax returns.

This naturally prompts the question – what exactly is a pass-through entity?

Understanding Pass-Through Entities

A pass-through entity is a business structure where the income is directly funneled to the owners, shareholders, or investors – the individual partner’s share (or the beneficiary’s share). This implies that only these partners bear the tax responsibility on this income, not the entity itself.

Pass-through entities are frequently employed to circumvent double taxation. (u.s. returrn of partnership income)

Here’s how it works:

The IRS levies taxes on individuals based on their earnings (income tax) and businesses based on their income (corporate tax). If the business structures itself as a pass-through entity, it can eschew corporate tax. The reason is that the gross income of these entities is viewed solely as the income of the individual partners – the investors, owners, or shareholders. In other words, the earnings and the accompanying tax liability “pass-through” or “flow-through” to each individual.

Consequently, the partners pay taxes on business entities (income) as if it were their income, at their usual income rate. These structures result in pass-through taxation. Furthermore, the partners can offset the company’s losses against their income. More on this discussion about depreciation.

While pass-through entities are subject to the same tax laws as C corporations regarding accounting, depreciation, and other factors impacting profit measurement, they are taxed only once.

Contrastingly, income generated through C corporations is subject to double taxation. Initially at the corporate tax rate and subsequently when dividends are distributed to shareholders or when shareholders realize capital gains from retained earnings.

The Role of Form K-1

The K-1 Centers around Real Estate Syndications. If you are still getting familiar with Syndications, click the video below.

Syndications are investments wherein multiple investors, both general and limited partners, combine their resources to invest in a property.

The general partner (GP) or sponsor manages the property, makes informed decisions, and oversees the day-to-day operations.

The limited partners (LPs), or passive investors, inject capital but refrain from actively engaging in property management.

Syndications are typically structured as either:

- Limited Partnerships (LPs)

- Limited Liability Companies (LLCs) Both structures qualify as pass-through entities from a tax perspective.

Responsibilities

Each passive investor is individually responsible for their share of tax obligations, as the syndication partnership is not taxable.

The sponsors compile each limited partner’s K1 tax form, detailing their portion of the syndication’s income, losses, and other tax-related factors, such as depreciation and deductions associated with the property’s expenses.

These details are then included in their individual tax returns (Form 1040) for all the individual owners.

Timelines

Timing of K1s Issuance by Sponsors If you are a limited partner in syndication or another pass-through entity, you should expect to receive your K-1s from the sponsor by the 15th day of the third month following the end of the tax year.

For instance, if the calendar year concluded on December 31, 2022, you should receive your Schedule K-1 by March 15, 2023.

Parts of Form K-1

Compiling and filing the partnership return can be complex, necessitating multiple professionals’ expertise to ensure the information’s accuracy and maximize available deductions.

There may be scenarios where the filing process becomes exceedingly intricate, warranting a filing extension that could delay the receipt of K-1s for LPs. If this arises, maintain open communication channels with your investment sponsor to stay updated on the anticipated timelines for the K-1.

How to Interpret a K-1 (Form 1065) K-1 forms are divided into three segments:

- Part I: Partnership information

- Part II: Information about the partner or shareholder

- Part III: Partner’s or shareholder’s proportion of current year income, deductions, credits, and other items. Let’s delve deeper into each section.

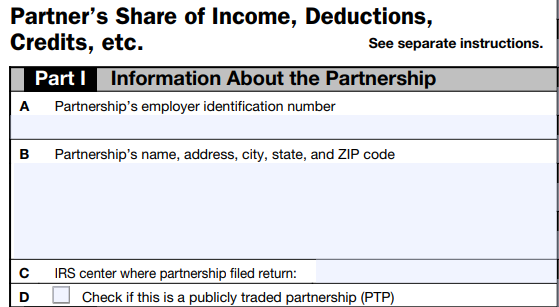

Part I

Here’s Part 1 of a blank K-1 form

This section includes details about the partnership, such as:

- Employer Identification Number (EIN) number.

- Name and complete address

- Number of shares (for corporations) As the limited partner, you don’t need to worry about filling out this form, as it’s the responsibility of the entity issuing it to you. When you review this section, ensure that the partner’s name and information match yours to verify that you’ve received the correct K-1 form for the appropriate investment.

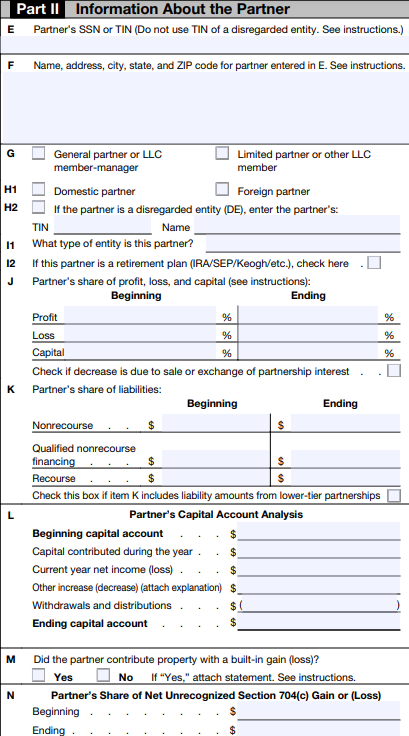

Part II

This segment features your details as the investor, including:

- SSN or TIN

- Name and complete address

- Number of shares and loans (for corporations)

- Type of partner, losses, and shares (for partnerships) Ensure this information is accurate, especially if there have been changes like a new address

- Initial balance

- Any capital contributed by you

- Increases resulting in your final balance Again, verify this information for accuracy to avoid being taxed on gains that weren’t yours.

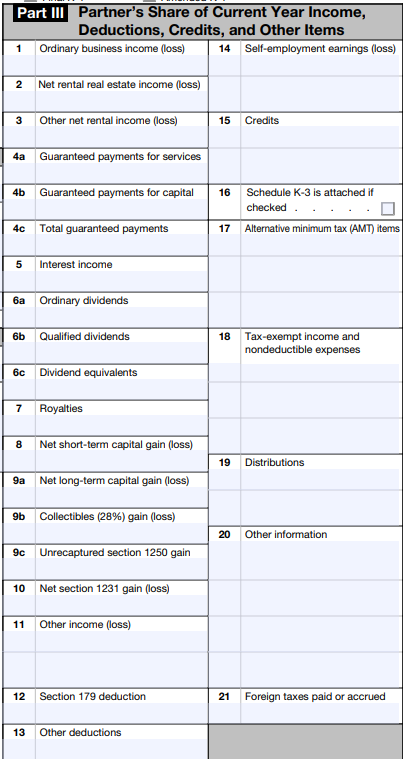

Part III

Box 2 details the net real estate income gain or loss, reflecting the profit or loss accrued by the Limited Partner (LP) according to their ownership percentage. This net amount is computed by subtracting expenses from revenue and adding any depreciation obtained from the property.

In most syndications I’ve participated in, a “net rental real estate loss” is expected because the depreciation from the cost segregation study typically surpasses the net income. Hence, there may be a loss (negative figure in Box 2) even if the LP received distributions during the year, reflected in Box 19.

New investors often misconstrue this negative figure as a sign of underperformance, believing they’ve lost capital. But that isn’t the case. This figure merely mirrors their share of the “paper loss” due to depreciation.

The depreciation-induced loss enables us, the limited partners, to reduce our taxable income. This provides a tremendous tax benefit, sometimes even making the distributions received tax-free.

Here are other crucial boxes to review:

- Box 4: Portfolio interest income

- Box 5: Dividends

- Box 7: Royalties

- Box 8: Short-term capital gains

- Box 9a: Long-term capital gains

- Box 9b: Collectibles (28%) gain (loss)

- Box 10: Net Section 1231 gain (loss)

- Box 11: Other income (loss)

- Box 12: Section 179 deduction

- Box 13: Other deductions

- Box 14: Self-employment earnings (loss)

- Box 15: Credits

- Box 16: Foreign transactions

- Box 17: Alternative minimum tax (AMT) items

- Box 18: Tax-exempt income and nondeductible expenses

- Box 19: Distributions Box 20: Other information

Always consult with your tax professional or preparer when interpreting the K-1 document.

Frequently Asked Questions

Yes, you need to include the information from a K1 on your tax returns. The K-1 form is a tax document which outlines your ownership stake, share of income, deductions, credits, and other items from the partnership, S corporation, or estate/trust.

The partnership, S corporation, or estate/trust is responsible for preparing and issuing K1 forms to their partners or shareholders.

A 1099 form reports various types of income (interest, dividends, freelance payments) earned by an individual or small business. A K1, in contrast, reports a partner’s or shareholder’s share of income, deductions, credits, and other items from a partnership, S corporation, or estate/trust.

Typically, K1 income is taxed at the individual partner’s ordinary income tax rate. However, the exact tax treatment can vary depending on the type of income, deductions, credits, or other items reported on the K1.

Refrain from filing a K-1 form with your tax returns to avoid penalties and possibly an IRS audit because you have underreported your taxable income.

Summing It Up As an investor who wants to become a limited partner in syndications, understanding the K-1 form is crucial as it records your share of the partnership’s income, losses, deductions, and credits. Consider this guide a handy resource each time you receive your K-1 tax form.

Always consult with a financial advisor, CPA, or CFP to make sure your financial plans align with your goals, risk tolerance and financial situation.

–