Leaders entering a new role encounter a pivotal juncture that significantly shapes their long-term success within the organization. Michael D. Watkins, a prominent figure in leadership development, emphasizes the critical nature of the first 90 days in establishing a firm foundation for executives in their new job.

The Significance of the First 90 Days:

[divi_switch_layout id=”1311″]

During this period, making a positive first impression and securing early wins is paramount. Watkins highlights the profound impact of initial actions on shaping perceptions, drawing on the insights of social psychologist Amy Cuddy. Building trust and respect is foundational as leaders forge new professional relationships, laying the groundwork for future challenges and successes.

Navigating the First-Time Manager Status

The Complexity of Early Win Projects:

Leaders, often stepping into their first-time manager roles, must strategically approach projects aimed at achieving early wins. Watkins underscores the importance of aligning personal victories with organizational objectives, stressing that first actions should not only resonate positively with the team but also contribute meaningfully to the company’s organizational structure.

As leaders navigate their first day and subsequent weeks, the focus on making a positive first impression becomes critical. The 90-day plan extends beyond a mere survival guide; it’s an opportunity to build trust and understanding. Drawing on insights from Amy Cuddy, this section explores the psychological aspects of trust formation and the pivotal role leaders play in fostering a positive and productive work environment.

Join our passive investor clubhere and embark on a collective path to real estate success.

Strategic Alignment and Goal Definition

Defining Success in a New Leadership Role

Establishing Clear Expectations:

New leaders shoulder the responsibility of not only understanding their new position but also aligning their goals with the broader vision of the organization. Clear expectations become the cornerstone of a successful transition. Watkins advocates for transparent conversations with supervisors and key stakeholders to delineate success criteria and personal development expectations.

Navigating the Company Hierarchy:

Leadership roles demand a nuanced understanding of the company’s hierarchy. It’s imperative for executives to comprehend the expectations of both their direct reports and superiors. Aligning goals along the chain of command ensures a cohesive approach, where each echelon comprehends the overarching vision for success. Watkins illustrates this through practical examples, emphasizing the need for synchronization in defining success metrics.

Adapting to Organizational Dynamics

Addressing Challenges in Various Organizations:

Watkins introduces the concept of STARS (Startup, Turnaround, Accelerated Growth, Realignment, and Sustaining Success) to underscore the diverse challenges leaders face in different organizational types. Whether steering through the tumultuous phases of a startup or navigating the delicate balance of a sustaining success scenario, understanding the unique dynamics is vital for effective leadership. This section delves into practical strategies tailored to each organizational type.

Strategic Decision-Making for Long-Term Success:

Leadership transitions are marked by significant decisions, and Watkins underscores the need for strategic decision-making. Aligning with the company’s vision, understanding the organizational culture, and considering international best practices are crucial. Leaders are urged to leverage resources like the International Institute for Management Development and tap into the expertise of organizations like Genesis Advisers for effective decision-making.

The Art of Communication and Relationship-Building:

A critical success factor for leaders is the ability to communicate effectively. This involves not only conveying clear expectations but also nurturing relationships within and outside the organization. Watkins introduces the concept of a road map for communication, guiding leaders on the right direction. Building strong relationships and alliances, especially during the initial days, is identified as a key element in the successful leadership playbook.

Tailoring Strategies for Organizational Success

Adapting Leadership Approaches to Different Organizational Types

STARS Framework: A Blueprint for Success:

Watkins introduces the STARS acronym, a pivotal framework for leaders to understand the nature of their new organization. Whether it’s a Startup, Turnaround, Accelerated Growth, Realignment, or Sustaining Success, each type demands a tailored approach. Leaders are advised to carefully analyze the organization’s position and challenges, aligning their strategies with the specific requirements of the STARS type.

Organizational Structure Alignment:

A significant aspect of leadership transitions is evaluating and adjusting the organizational structure. Watkins identifies four core elements crucial for success: strategic direction and vision, skill sets, organizational units and work processes, and their respective rewards. Leaders are encouraged to bring alignment to these elements to ensure the organization is poised for success.

Implementing Change: The Right Way:

While major changes might be necessary, Watkins stresses the importance of understanding the status quo before implementing any shifts. Leaders should resist the urge for immediate action and instead focus on learning and understanding the company’s dynamics. This involves holding structured one-on-one meetings, implementing a learning process, and gathering essential insights before proposing changes.

Building a Culture of Success:

Leadership transitions provide an opportunity to shape the company culture for long-term success. By fostering an environment where each employee is aligned with the vision of success, leaders contribute to the creation of a positive and motivated workforce. Watkins underlines the importance of understanding the nuances of the company’s goals and standards, ensuring everyone, from direct reports to senior leaders, shares a common vision.

The concept of early wins is revisited, emphasizing the need for leaders to secure victories that align with the organization’s STARS type. Rather than pursuing superficial victories, leaders should aim for strategic wins that contribute to the company’s overall success. This involves careful consideration of the company’s goals and priorities, ensuring that early wins set the stage for long-term positive momentum.

Navigating the Leadership Landscape: Challenges and Solutions

Understanding the Challenges of Leadership Transitions:

Leadership transitions are not without their challenges, and Watkins delves into the intricacies of the learning curve that leaders often face. The transition period can be marked by a series of adjustments, and leaders are advised to approach it with humility, recognizing that what worked in a previous role might not apply universally. Acknowledging the uniqueness of each organizational setting and its challenges is crucial for making good decisions during the initial phase.

Overcoming Vicious Cycles:

Watkins sheds light on the concept of vicious cycles that leaders might encounter, emphasizing the importance of breaking free from detrimental patterns. These cycles can hinder progress and create roadblocks for leaders aiming for a successful transition. Recognizing these cycles and adopting a strategic approach to disrupt them is essential for steering the ship in the right direction.

The Role of Clear Expectations:

Clear expectations play a pivotal role in successful leadership transitions. Leaders should engage in open and transparent communication with key stakeholders, understanding their expectations and aligning them with the organizational goals. This involves creating a comprehensive road map that outlines critical success strategies and sets the right expectations for both the leader and the team.

The Impact of Leadership Style:

Watkins emphasizes the significance of a leader’s leadership style in influencing the dynamics of a team. Leaders should be conscious of their approach, recognizing that different situations might require different leadership styles. Whether it’s a nurturing style for a team in need of support or a more directive style for a team in a crisis, adapting the leadership approach can contribute to a smoother transition.

Beyond the organizational aspects, leadership transitions offer an opportunity for both personal and professional growth. Leaders are encouraged to view each transition as a chance to enhance their skills, broaden their perspectives, and prepare for the next move in their career. Watkins underscores the importance of continuous learning and development throughout a leader’s journey.

Insights from a Noted Expert:

As a co-founder of Genesis Advisers and a Professor of Leadership and Organizational Change at the International Institute for Management Development, Michael D. Watkins brings a wealth of expertise to the discussion. Drawing on his experiences and research, Watkins provides valuable insights into the intricacies of leadership transitions, offering a comprehensive guide for leaders navigating these critical periods in their careers.

Success Summary: The First 90 Days Book Review

Building Strong Foundations: The First 90 Days Approach

Crafting a Solid 90-Day Plan:

Watkins introduces the concept of the crucial 90-day plan, emphasizing its significance in shaping a leader’s initial actions. This period is not merely about making a positive first impression but involves a strategic approach to learning, understanding, and setting the stage for long-term success. Leaders are advised to resist the “action imperative” and focus on building a foundation through careful planning and assessment.

Strategic Importance of First Impressions:

The first 90 days set the tone for a leader’s tenure, and Watkins highlights the strategic importance of making a positive first impression. Drawing on the insights of social psychologist Amy Cuddy, he underscores that trust and respect are at the core of professional relationships. Leaders should be mindful of the impressions they create, as these early perceptions can have a lasting impact on their ability to lead effectively.

Establishing Early Wins:

Watkins introduces the concept of early wins, noting their significance in building credibility and momentum. Leaders should aim for victories that align with the organization’s goals and address its specific challenges. However, the pursuit of early wins requires a nuanced understanding of the organizational structure, the expectations of key stakeholders, and the unique dynamics of the team.

Adapting to Organizational STARS Types:

Leadership transitions involve adapting to different organizational contexts, and Watkins introduces the STARS acronym—Startup, Turnaround, Accelerated Growth, Realignment, and Sustaining Success. Understanding which category defines the new organization is crucial for tailoring strategies effectively. Each type presents distinct challenges, and successful leaders tailor their approaches based on the specific demands of the organizational context.

Alignment of Organizational Structure:

Watkins explores the critical role of aligning the organizational structure for success. Leaders may need to make structural changes within the first 90 days to ensure key elements such as strategic direction, skill sets, organizational units, and work processes are in harmony. This alignment is pivotal for optimizing the efficiency of the entire organization and positioning each employee for success.

Building a Cohesive Team:

Success in a new leadership role hinges on the ability to build a cohesive team. Watkins provides insights into understanding team members, assessing their performance, and cultivating strong relationships. Leaders are urged to go beyond surface-level evaluations, delving into the reasons behind performance levels and adopting a thoughtful approach to team dynamics.

Guidance for New Leaders:

Drawing on his extensive experience, Michael D. Watkins offers practical advice for leaders navigating the complexities of their first 90 days. This section serves as a guide for those stepping into new roles, providing actionable insights to make the transition smoother and set the stage for a successful leadership journey.

Navigating Challenges and Key Strategies for Success

Overcoming the Learning Curve:

One of the primary challenges faced by leaders in their new role is the steep learning curve. Watkins acknowledges that transitions involve adapting to new environments, cultures, and expectations. Leaders, especially those stepping into a management role for the first time, need to recognize the value of continuous learning and be proactive in seeking insights that contribute to their future success.

Decoding Leadership Styles:

Watkins delves into the significance of understanding and defining one’s leadership style. He emphasizes that a successful leader aligns their style with the organizational culture, goals, and the expectations of key stakeholders. The ability to adapt and flex one’s leadership approach based on the situation contributes to building strong relationships and effectively guiding the team.

Strategic Decision-Making:

Leadership transitions necessitate making a series of decisions that impact the team and the organization. Watkins underscores the importance of making good decisions and provides guidance on navigating through different situations. Decision-making is not only about choosing the right direction but also involves considering the long-term implications and ensuring alignment with organizational goals.

Adapting to Different Situations:

Successful leaders recognize that each transition is unique, and they must adapt their approach to different situations. Whether it’s a shift in organizational structure, a change in team dynamics, or a new strategic direction, leaders need to be agile and responsive. Watkins offers insights into how leaders can navigate varied scenarios with resilience and effectiveness.

Cultivating Strong Relationships:

Building strong relationships is a cornerstone of successful leadership. Watkins advises leaders to go beyond their direct reports and foster alliances across the organization. Understanding the importance of key stakeholders and forming positive connections contributes to a leader’s influence and ability to implement meaningful changes.

Managing Career Transitions:

Leadership transitions often involve not just a new job but an evolution in one’s career. Watkins explores how individuals can manage their career transitions effectively, whether it’s moving into a more senior role, taking on new responsibilities, or transitioning to a different company. Strategic planning and thoughtful decision-making play a crucial role in shaping a fulfilling and successful career trajectory.

Strategies for Effective Change:

Watkins provides insights into the complexities of implementing major changes within an organization. Leaders are guided on how to navigate the challenges of disrupting the status quo, breaking free from vicious cycles, and driving meaningful transformation. Successful change management involves a combination of strategic planning, effective communication, and a deep understanding of the organizational dynamics.

Maintaining a Positive Organizational Culture:

The importance of company culture in sustaining long-term success is highlighted by Watkins. Leaders are encouraged to be proactive in shaping and preserving a positive organizational culture. This involves aligning the team with the company’s values, fostering open communication, and establishing a workplace environment that promotes collaboration and innovation.

Strategic Goal Setting:

Watkins emphasizes the significance of clear expectations and strategic goal setting. Leaders, both new and experienced, need to establish a road map for success, defining the critical success strategies that align with the organization’s overall vision. This proactive approach ensures that the team is focused on shared goals and is working collectively toward achieving them.

Striking the Right Balance:

The transition into a new leadership role involves juggling various responsibilities and expectations. Watkins provides insights into striking the right balance between work and personal life. A successful leader recognizes the importance of maintaining a healthy work-life balance, ensuring sustained performance and well-being.

Evaluating Past Jobs and Gaining Insight:

Reflecting on past jobs is a valuable exercise for leaders transitioning into a new role. Watkins explores how leaders can gain valuable insights from their previous experiences, both successes, and challenges. This reflective process contributes to continuous improvement and enhances the leader’s ability to make informed decisions in their current role.

Strategic Networking and Alliances:

Watkins underscores the role of networking and forming strategic alliances in a leader’s success journey. Leaders are encouraged to leverage their connections, both within and outside the organization, to gain insights, share experiences, and stay informed about industry trends. Strategic networking enhances a leader’s visibility and influence within their professional ecosystem.

Preparing for the Next Move:

The dynamic nature of careers requires leaders to be forward-thinking. Watkins provides guidance on how leaders can strategically position themselves for their next move. Whether it’s within the same organization, a shift to a different industry, or the pursuit of higher leadership roles, preparing for the next move involves a proactive and strategic approach.

Achieving Break-Even Point:

Watkins introduces the concept of the break-even point in a leader’s journey. This is the juncture where leaders have contributed as much value to the organization as they have received in education and onboarding. Achieving this equilibrium is a key milestone in a leader’s career, signifying their successful integration into the organizational fabric.

Unlocking the Potential of Direct Reports:

Leaders are urged to recognize the potential of their direct reports and play a proactive role in unlocking their capabilities. Watkins provides insights into how leaders can inspire, mentor, and guide their team members toward achieving their best. Investing in the professional development of direct reports contributes to overall team success and strengthens the leader’s legacy.

Future Success through Continuous Improvement:

Watkins emphasizes the importance of embracing a mindset of continuous improvement for future success. Leaders should be open to learning, adapting, and evolving their strategies based on feedback and changing circumstances. This commitment to ongoing improvement positions leaders as dynamic and resilient contributors to the long-term success of their organizations.

Strategic Management Development:

The role of management development in shaping successful leaders is explored by Watkins. Leaders should actively engage in their own development, seeking opportunities for growth and enhancement of their skills. Additionally, cultivating a culture of continuous learning and development within the organization contributes to the overall success and adaptability of the leadership team.

Watkins concludes by reiterating the significance of a well-planned and thoughtful approach to leadership transitions. The first 90 days serve as a critical period for leaders to establish their presence, build trust, and set the stage for long-term success. By embracing practical strategies, adapting to unique organizational contexts, and maintaining a commitment to continuous improvement, leaders can navigate transitions successfully and leave a lasting positive impact on their teams and organizations.

Navigating Challenges and Key Strategies for Success

Success Summary: The First 90 Days Book Review

Overcoming the Learning Curve:

One of the primary challenges faced by leaders in their new role is the steep learning curve. Watkins acknowledges that transitions involve adapting to new environments, cultures, and expectations. Leaders, especially those stepping into a management role for the first time, need to recognize the value of continuous learning and be proactive in seeking insights that contribute to their future success.

Decoding Leadership Styles:

Watkins delves into the significance of understanding and defining one’s leadership style. He emphasizes that a successful leader aligns their style with the organizational culture, goals, and the expectations of key stakeholders. The ability to adapt and flex one’s leadership approach based on the situation contributes to building strong relationships and effectively guiding the team.

Strategic Decision-Making:

Leadership transitions necessitate making a series of decisions that impact the team and the organization. Watkins underscores the importance of making good decisions and provides guidance on navigating through different situations. Decision-making is not only about choosing the right direction but also involves considering the long-term implications and ensuring alignment with organizational goals.

Adapting to Different Situations:

Successful leaders recognize that each transition is unique, and they must adapt their approach to different situations. Whether it’s a shift in organizational structure, a change in team dynamics, or a new strategic direction, leaders need to be agile and responsive. Watkins offers insights into how leaders can navigate varied scenarios with resilience and effectiveness.

Cultivating Strong Relationships:

Building strong relationships is a cornerstone of successful leadership. Watkins advises leaders to go beyond their direct reports and foster alliances across the organization. Understanding the importance of key stakeholders and forming positive connections contributes to a leader’s influence and ability to implement meaningful changes.

Managing Career Transitions:

Leadership transitions often involve not just a new job but an evolution in one’s career. Watkins explores how individuals can manage their career transitions effectively, whether it’s moving into a more senior role, taking on new responsibilities, or transitioning to a different company. Strategic planning and thoughtful decision-making play a crucial role in shaping a fulfilling and successful career trajectory.

Strategies for Effective Change:

Watkins provides insights into the complexities of implementing major changes within an organization. Leaders are guided on how to navigate the challenges of disrupting the status quo, breaking free from vicious cycles, and driving meaningful transformation. Successful change management involves a combination of strategic planning, effective communication, and a deep understanding of the organizational dynamics.

Maintaining a Positive Organizational Culture:

The importance of company culture in sustaining long-term success is highlighted by Watkins. Leaders are encouraged to be proactive in shaping and preserving a positive organizational culture. This involves aligning the team with the company’s values, fostering open communication, and establishing a workplace environment that promotes collaboration and innovation.

Strategic Goal Setting:

Watkins emphasizes the significance of clear expectations and strategic goal setting. Leaders, both new and experienced, need to establish a road map for success, defining the critical success strategies that align with the organization’s overall vision. This proactive approach ensures that the team is focused on shared goals and is working collectively toward achieving them.

Striking the Right Balance:

The transition into a new leadership role involves juggling various responsibilities and expectations. Watkins provides insights into striking the right balance between work and personal life. A successful leader recognizes the importance of maintaining a healthy work-life balance, ensuring sustained performance and well-being.

Evaluating Past Jobs and Gaining Insight:

Reflecting on past jobs is a valuable exercise for leaders transitioning into a new role. Watkins explores how leaders can gain valuable insights from their previous experiences, both successes, and challenges. This reflective process contributes to continuous improvement and enhances the leader’s ability to make informed decisions in their current role.

Strategic Networking and Alliances:

Watkins underscores the role of networking and forming strategic alliances in a leader’s success journey. Leaders are encouraged to leverage their connections, both within and outside the organization, to gain insights, share experiences, and stay informed about industry trends. Strategic networking enhances a leader’s visibility and influence within their professional ecosystem.

Preparing for the Next Move:

The dynamic nature of careers requires leaders to be forward-thinking. Watkins provides guidance on how leaders can strategically position themselves for their next move. Whether it’s within the same organization, a shift to a different industry, or the pursuit of higher leadership roles, preparing for the next move involves a proactive and strategic approach.

Achieving Break-Even Point:

Watkins introduces the concept of the break-even point in a leader’s journey. This is the juncture where leaders have contributed as much value to the organization as they have received in education and onboarding. Achieving this equilibrium is a key milestone in a leader’s career, signifying their successful integration into the organizational fabric.

Unlocking the Potential of Direct Reports:

Leaders are urged to recognize the potential of their direct reports and play a proactive role in unlocking their capabilities. Watkins provides insights into how leaders can inspire, mentor, and guide their team members toward achieving their best. Investing in the professional development of direct reports contributes to overall team success and strengthens the leader’s legacy.

Future Success through Continuous Improvement:

Watkins emphasizes the importance of embracing a mindset of continuous improvement for future success. Leaders should be open to learning, adapting, and evolving their strategies based on feedback and changing circumstances. This commitment to ongoing improvement positions leaders as dynamic and resilient contributors to the long-term success of their organizations.

Strategic Management Development:

The role of management development in shaping successful leaders is explored by Watkins. Leaders should actively engage in their own development, seeking opportunities for growth and enhancement of their skills. Additionally, cultivating a culture of continuous learning and development within the organization contributes to the overall success and adaptability of the leadership team.

Watkins concludes by reiterating the significance of a well-planned and thoughtful approach to leadership transitions. The first 90 days serve as a critical period for leaders to establish their presence, build trust, and set the stage for long-term success. By embracing practical strategies, adapting to unique organizational contexts, and maintaining a commitment to continuous improvement, leaders can navigate transitions successfully and leave a lasting positive impact on their teams and organizations.

In the dynamic realm of real estate investment, Bridgestone Capital stands as a beacon, specializing in the acquisition of commercial properties. Focused on forging strategic collaborations, Bridgestone Capital invites investors into a realm where the complexities of property management are seamlessly navigated. At the heart of this operation lies a commitment to safeguarding investments, and a cornerstone in achieving this goal is the meticulous process of commercial building inspections.

As guardians of a diverse portfolio, Bridgestone Capital recognizes that the foundation of a successful real estate venture lies not only in the acquisition of commercial properties but also in understanding the critical role that commercial building inspections play in protecting these investments.

The subsequent sections will delve into the intricacies of commercial building inspections, from their definitions and legal requirements to the comprehensive coverage they offer. If you have any specific details or preferences you’d like to include, feel free to share, and I’ll ensure they are incorporated.

Understanding Commercial Building Inspections

Definition and Purpose of Inspections

In the intricate dance of real estate transactions, the role of a skilled inspector becomes paramount. Whether it’s a residential home inspection or a comprehensive evaluation of sprawling commercial properties, the inspector serves as the discerning eye, unraveling the mysteries that lie within the walls.

For commercial properties, the stakes are high, and the demand for a professional commercial inspector is non-negotiable. These seasoned inspectors specialize in navigating the unique nuances of office buildings, considering not only the major systems like HVAC and electrical systems but also the sprawling parking lots and intricate structural configurations.

A thorough inspection is not just a routine task; it’s a strategic investment in the long-term health of a property. Beyond the square footage and the impressive facades of office spaces, a commercial inspector digs deeper. They assess the structural integrity of the building, scrutinize the condition of parking lots, and inspect the HVAC systems that silently contribute to the comfort within.

In the commercial landscape, where every decision can impact potential buyers and the sale price of a property, a meticulous inspector provides more than peace of mind – they offer a roadmap for informed decisions. A commercial property inspector, armed with decades of experience, becomes a critical asset, identifying critical issues in older buildings and pinpointing potential hazards that could lead to costly repairs.

As property owners navigate the complexities of commercial real estate, a professional inspector becomes a guide, ensuring that every inch of the property is scrutinized for condition, compliance with local building codes, and adherence to safety standards. The inspector’s findings are not just a report; they are a strategic tool for property owners, a comprehensive resource that aids in decision-making for the meticulous care of valuable investments.

In the world of commercial real estate, where the best time for an inspection can significantly impact the property’s future, a skilled commercial inspector is the answer. Their expertise goes beyond a mere hourly rate; it encompasses a commitment to a comprehensive approach, a dedication to understanding the specific needs of each type of structure, and the diligence required to unearth potential problems before they escalate.

In the next sections, we’ll delve into the legal requirements of inspections, explore the various types of inspections available, and uncover the extensive coverage provided by a commercial building inspection. These sections will shed light on the meticulous process that goes into safeguarding commercial properties and ensuring they stand the test of time.

[divi_switch_layout id=”1311″]

What a Commercial Building Inspection Covers

Structural and Mechanical Systems

In the intricate tapestry of a commercial building, the structural and mechanical systems are the unsung heroes, ensuring the stability and functionality of the entire structure. A comprehensive commercial building inspection places these systems under the microscope, examining every facet from foundation to framing.

The structural integrity of a building is a critical factor that influences its longevity. A skilled commercial building inspector, often armed with the insights of a structural engineer, meticulously assesses the foundation, framing, and overall stability. Years of experience play a crucial role in identifying subtle signs that could develop into major concerns in the long run.

Beyond the skeletal framework, the inspection encompasses the mechanical systems that breathe life into a commercial property. Heating, ventilation, and air conditioning (HVAC) systems are scrutinized for efficiency, ensuring they not only maintain a comfortable environment but also operate in a manner that doesn’t pose safety hazards to occupants.

Electrical & Plumbing Systems

The nerve center of any commercial property lies within its electrical and plumbing systems. A commercial building inspection dives deep into these critical components, ensuring that the complex web of wiring and piping is not just functional but meets the stringent standards required for a safe and reliable environment.

Electrical systems are evaluated for potential hazards, addressing issues such as improper wiring installations that could lead to safety concerns. Plumbing systems, vital for maintaining a safe and healthy environment, undergo thorough checks to prevent disruptions like clogged drains or sewer backups that could impact business operations.

Environmental Factors (e.g., Asbestos, Mold)

The commercial building inspection process extends beyond the visible structures to address hidden threats lurking in environmental factors. Older buildings, in particular, may harbor hazardous materials like asbestos, known for its potential health risks. A certified commercial inspector, well-versed in property condition assessments, identifies these materials and provides recommendations for safe removal or containment.

Mold, another environmental concern, thrives in damp conditions and poses risks to respiratory health. The inspector’s keen eye detects signs of mold growth, such as discoloration or musty odors, ensuring a proactive approach to maintaining a healthy indoor environment.

ADA Compliance

Ensuring accessibility for everyone, including individuals with disabilities, is not just an ethical consideration but a legal necessity. A commercial building inspection meticulously checks for compliance with the Americans with Disabilities Act (ADA), covering aspects like ramping, parking accessibility, and door widths. Failing to adhere to these regulations not only invites potential legal consequences but also hinders the seamless operation of commercial spaces.

In the next section, we’ll explore the vital considerations in choosing the right commercial building inspector. The qualifications, certifications, experience, and reputation of an inspector play a pivotal role in the efficacy of the inspection process.

[divi_switch_layout id=”1311″]

Choosing the Right Commercial Building Inspector

When it comes to choosing a commercial building inspector, the stakes are high. The qualifications, certifications, experience, and reputation of an inspector can significantly impact the outcome of the inspection process.

Qualifications & Certifications

Not all inspectors are created equal, and for commercial properties, it’s crucial to seek out professionals with specialized training and certifications. The American Society of Home Inspectors (ASHI) or the International Association of Certified Home Inspectors (InterNACHI) are reputable organizations that offer certifications specific to commercial inspections.

A quality inspection demands an inspector who understands the nuances of commercial properties, from office buildings to residential units. Their expertise in different constants, such as the type of structure being inspected and the specific regulations governing it, ensures a thorough evaluation.

See one of our properties 1 year after takeover!

Assessing Experience & Reputation

Experience is a cornerstone in the realm of commercial building inspections. An inspector with a track record of working on similar properties brings valuable insights that might escape less seasoned professionals. The nuances of inspecting diverse building types, whether they are residential properties or structures designed for commercial purposes, require a seasoned eye.

Reputation matters in the inspection business. Positive reviews from previous clients and recommendations from industry professionals serve as indicators of an inspector’s reliability. Requesting references or reviewing past inspection reports can offer a glimpse into the inspector’s commitment to quality and attention to detail.

Communication & Reporting

The inspection process is not solely about the physical examination; effective communication is equally vital. When choosing a commercial building inspector, consider their ability to convey complex information in a clear and concise manner. Timely updates throughout the inspection and a comprehensive final report are hallmarks of a professional inspector.

A quality inspection report should cover all areas of the building examined, including photos or diagrams where necessary. It acts as a valuable document for property owners, investors, and portfolio managers, providing relevant information to make informed decisions about the property.

In the subsequent section, we’ll delve into the myriad benefits that regular commercial building inspections bring to property owners, investors, and tenants alike.

Benefits of Regular Commercial Building Inspections

Investing in regular commercial building inspections isn’t just a good practice; it’s a strategic move with multifaceted benefits for property owners, investors, and tenants. Let’s explore these advantages in detail:

Prevention of Potential Problems and Costly Repairs

Regular inspections serve as proactive guardians, identifying potential issues before they evolve into major problems. By spotting and addressing concerns early on, property owners can avoid costly repairs that may arise if problems escalate. It’s a cost-effective approach to property management, ensuring that minor issues are nipped in the bud, ultimately saving money in the long run.

For property owners, investors, and tenants, protecting their investment is a shared priority. Regular commercial building inspections play a pivotal role in ensuring the longevity and value of commercial properties. By identifying potential maintenance issues early on, necessary repairs can be made before they escalate into major problems, potentially resulting in costly repairs or legal consequences.

Compliance with Building Codes and Regulations

Staying abreast of building codes and regulations is not just a legal obligation; it’s a fundamental aspect of responsible property ownership. Regular commercial building inspections help ensure compliance, reducing the risk of fines and legal troubles. This commitment to meeting industry standards creates a safe environment, preventing potential hazards and ensuring the longevity of the property.

Assurance of Safety for Employees and Customers

Prioritizing safety is paramount for any commercial property owner. Regular inspections offer assurance that the building is up-to-date with safety requirements and regulations. By identifying potential hazards like faulty wiring or structural issues, necessary repairs can be made promptly, reducing liability risks. A safe environment not only protects individuals within the building but also contributes to maintaining a positive business reputation.

Protection of Investment

In the final section, we’ll discuss essential steps in preparing for a commercial building inspection, underlining the significance of a well-organized and proactive approach.

[divi_switch_layout id=”1311″]

How to Prepare for a Commercial Building Inspection

Preparing for a commercial building inspection is a strategic process that ensures a thorough evaluation of the property. Here are essential steps to streamline the inspection process and make it as effective as possible:

Gathering Necessary Documents and Records

A well-organized documentation system is the cornerstone of a smooth inspection. Before the inspector arrives, gather all necessary documents related to the construction or renovation of the property. This includes permits, plans, blueprints, and any relevant paperwork that provides insight into the building’s structure and systems. Additionally, maintain records of past maintenance and repairs, including invoices, work orders, and receipts, to showcase the property’s maintenance history.

Making Necessary Repairs and Upgrades

Proactive measures go a long way in presenting the property in the best possible condition. Address any visible issues and make necessary repairs or upgrades before the inspection. This includes fixing plumbing leaks, repairing electrical systems, and ensuring the HVAC system is in optimal condition. Pay special attention to the building’s exterior, as the first impression can significantly impact the inspector’s findings.

Addressing Any Safety Concerns

Safety is paramount. Address any safety concerns found during regular property assessments or noted by tenants. This includes fixing faulty wiring, repairing broken staircases or railings, and eliminating potential fire hazards. By addressing safety concerns promptly, property owners not only ensure the well-being of occupants but also demonstrate a commitment to maintaining a safe and secure environment.

Scheduling the Inspection at a Convenient Time

Collaborate with the inspector to schedule the assessment at a time that works for both parties. Ensure that all areas of the building, including storage rooms and electrical panels, are accessible. Clearing any debris or clutter from these areas can save time and ensure that no issues go unnoticed during the inspection. A collaborative approach helps prevent delays in receiving the inspection report and addressing any potential problems found by the inspector.

In the concluding section, we’ll recap the crucial role commercial building inspections play in real estate investment and encourage property owners and investors to prioritize these assessments.

Gain insights on achieving financial independence while working your W2 subscribe!

To receive information about passive income ideas please contact me at jeff.davis@bridgestoneinvest.com. We have syndications going on throughout the year.

Always consult with a financial advisor, CPA, or CFP to make sure your financial plans align with your goals, risk tolerance and financial situation.

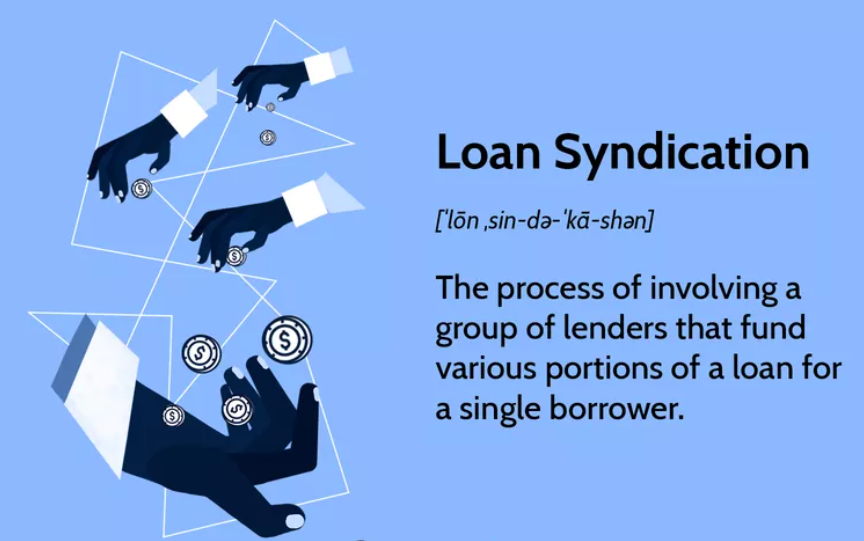

Real estate syndication has become a powerful tool for small businesses and real estate investors alike. At Bridgestone Capital, a private equity company specializing in commercial real estate in Texas, we understand the significance of comprehending the intricacies of real estate syndication structures. If you’re unfamiliar with the basics of syndication, you can find a comprehensive overview here.

This article delves into the legal, payout, and compensation structures integral to syndicated financing ventures. Join us as we explore the crucial aspects of real estate syndication structure that impact both general and limited partners. Remember, while this information provides valuable insights, it is not a substitute for legal advice. Always consult licensed securities and estate planning/asset protection attorneys before engaging in a real estate syndication deal.

Legal Considerations for Syndicated Financing

Real estate syndication, a dynamic financial strategy, necessitates a nuanced understanding of its legal underpinnings. At Bridgestone Capital, where we specialize in commercial real estate in Texas, we recognize the critical role legal considerations play in syndicated financing ventures.

Definition and Purpose

In essence, a real estate syndication is a collective endeavor where individuals pool resources to acquire property or fund a project. This collaborative approach, organized for a common purpose, brings both opportunities and responsibilities.

Choosing the Legal Entity Structure

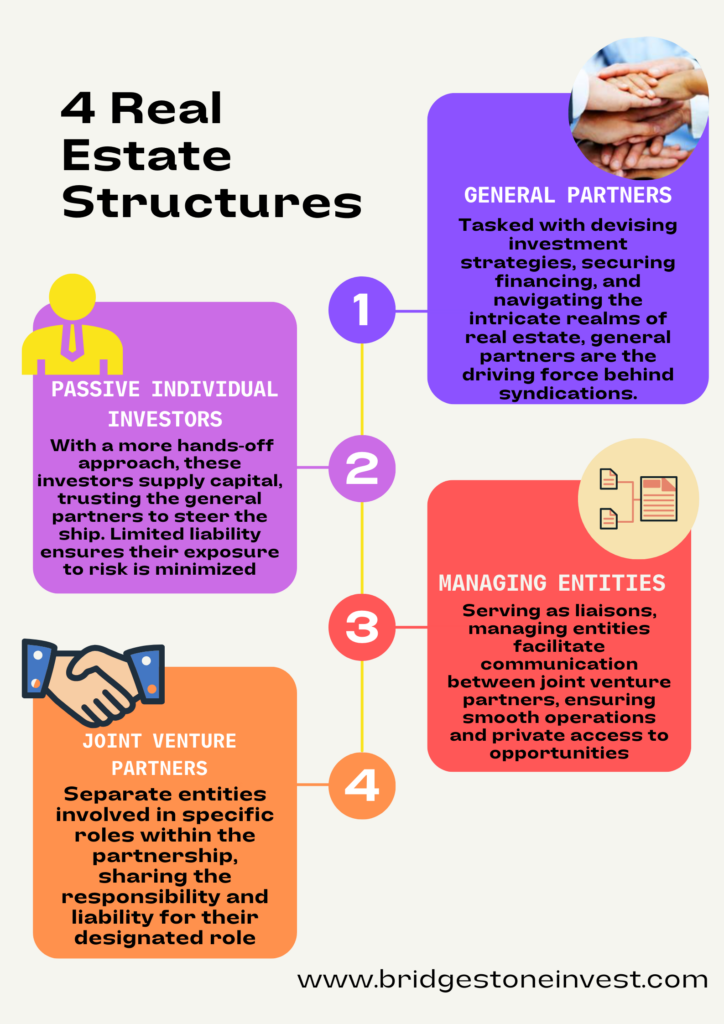

Determining the legal entity structure is a pivotal decision. Limited Partnership (LP) and Limited Liability Company (LLC) are the two primary choices, each with its merits. While LLCs offer flexibility in taxation and limited liability for members, LPs designate a general partner (GP) and limited partners (LPs) with distinct roles.

Considerations for investor roles and control are paramount. Limited partnerships provide a passive investing role, excluding investors from active management. The chosen structure should align with investors’ expectations regarding involvement.

Asset protection is a key facet, particularly for general partners. In an LP, GPs can be personally liable for debts, prompting many to form an LLC as the GP to mitigate such exposure.

Determination of Security Status

Understanding whether the syndication qualifies as a security is critical. The Supreme Court’s Howey Test offers a framework for assessment. An investment contract, as defined by the test, involves an investment of money in a common enterprise with an expectation of profits derived solely from the efforts of others.

Engaging with legal counsel is not just a recommendation but a necessity. The complexity of securities law requires expert guidance to navigate potential pitfalls and ensure compliance.

In the intricate tapestry of real estate syndication, these legal considerations weave the foundation for a successful venture. Always consult with seasoned securities and estate planning/asset protection attorneys before embarking on a real estate syndication journey.

Engaging with Investors

In the dynamic realm of real estate syndication, effective engagement with investors is a cornerstone of success. Bridgestone Capital, a leader in commercial real estate in Texas, recognizes the intricate dance between general partners (GPs) and investors in navigating this financial landscape.

Distinction between Accredited and Non-Accredited InvestorsUnderstanding the regulatory landscape is paramount, particularly the distinction between accredited and non-accredited investors. The Securities and Exchange Commission (SEC) categorizes investors based on their sophistication and financial thresholds. Accredited investors, deemed to possess a certain level of financial acumen, maintain specific earnings or net worth criteria.

Engaging with these distinct investor categories triggers different guidelines. GPs must be cognizant of SEC regulations governing offerings to accredited and non-accredited investors, influencing the type of SEC registration exemption they can file. This, in turn, dictates how they manage the project and structure the offering.

Responsibilities of General Partners

As a general partner, aligning with SEC guidelines is not just prudent; it’s imperative. Being accountable to different investor types requires a thorough understanding of their unique needs and expectations. General partners must tread carefully, ensuring compliance with securities laws and fostering transparency.

The Importance of Legal Counsel

Engaging investors involves more than financial acumen; it demands legal expertise. GPs should be adequately informed before entering a real estate syndication deal. Furthermore, limited partners should find assurance in the GP’s experience and legal counsel, ensuring that regulatory requirements are navigated with precision.

At Bridgestone Capital, we emphasize the significance of investor confidence. The alignment between a GP’s motivations and those of limited partners is vital. This principle guides our approach, fostering a trust-based relationship between syndicators and investors.

As we delve deeper into the intricacies of syndicated financing, it’s clear that legal considerations and investor engagement are symbiotic elements. Success in real estate syndication hinges on a delicate balance between regulatory adherence, transparent communication, and the cultivation of a mutually beneficial partnership.

[divi_switch_layout id=”1311″]

Engaging with Investors: Unlocking the Potential of Real Estate Syndication

Embarking on a journey into real estate syndication involves not just the identification of compelling investment opportunities, but also the strategic engagement of a diverse group of stakeholders. At Bridgestone Capital, a leader in commercial real estate in Texas, we recognize the significance of navigating this landscape with precision and expertise.

As a general partner (GP) leading a real estate syndication venture, your success hinges on understanding the varying dynamics within your investor base. From seasoned real estate investors to those taking their first step into a syndication deal, catering to a spectrum of investor profiles is crucial.

Structuring for Success

The choice between a limited partnership (LP) or a limited liability company (LLC) sets the foundation for your engagement strategy. Each structure has its nuances, influencing the roles and control afforded to investors. As you formulate a compelling deal structure, considering the preferences of passive investors and addressing their risk tolerance is key.

Due diligence is not only a phrase; it’s a commitment to providing potential investors with a clear understanding of the project’s risks, rewards, and intricacies. The development of a comprehensive business plan and a transparent private placement memorandum is the first step towards building investor confidence.

Appealing to Different Investor Types

Engaging with both accredited and non-accredited investors necessitates a tailored approach. Recognizing the guidelines set by the Securities and Exchange Commission (SEC) for different investor categories ensures compliance and effective communication. This awareness is especially vital when dealing with individual investors who may have varying levels of familiarity with real estate syndication.

Highlighting a successful track record and showcasing past performance becomes a cornerstone of your engagement strategy. Investors, whether seeking passive income or eyeing potential returns through capital gains, are drawn to a GP’s ability to execute a sound exit strategy.

While fees, such as the asset management fee and the acquisition fee, play a role in compensating GPs for their hard work, striking a balance is crucial. Communicating this effectively to investors ensures transparency and builds a foundation of trust.

Engaging with a diverse group of investors demands not only financial acumen but also an understanding of the human element. Beyond the transactional aspects, the success of real estate syndication hinges on the ability to align interests, communicate effectively, and foster trust within the investor community.

At Bridgestone Capital, we believe that a well-structured engagement strategy is the bedrock of successful real estate syndication. Join our community and explore the potential of syndicated financing as we navigate the nuances together.

Navigating Ownership and Compensation Structures in Real Estate Syndication

In the intricate journey of real estate syndication, the pivotal role of ownership and compensation structures takes the stage. Bridgestone Capital, a leader in commercial real estate in Texas, recognizes the profound impact these structures have on shaping the dynamics between general partners (GPs) and investors.

Exploring Compensation Architectures

Within the multifaceted realm of syndicated financing, various compensation structures govern ownership percentages and cash flow claims throughout the project’s lifecycle. This collaborative dance involves the syndication team and investors, emphasizing creativity and strategic design.

Key Compensation Structures:

Straight Split Syndications: This straightforward model ensures that cash flows and capital gains align with ownership percentages. Negotiations typically revolve around ratios like 50/50 (LP/GP) to 90/10 (LP/GP), influenced by the expertise brought in by the sponsor.

Preferred Return Structure: Prioritizing investor interests, this model guarantees a specified return on initial capital before the GP takes a share. Usually set between 6-8%, it establishes a baseline, with any excess compensation following a predetermined structure.

Distribution Waterfall: A sophisticated architecture dictating capital distribution, the waterfall progresses through tiers such as the return of capital (ROC), preferred return, GP catch-up, and carried interest. The latter is a predetermined percentage shared between investors and the sponsor.

Strategic Significance in Syndication

Beyond mere financial logistics, these compensation structures serve as blueprints guiding compensation dynamics throughout the project’s lifespan. More than financial considerations, the structure becomes the linchpin aligning GP motivations with those of limited partners, fostering a shared commitment to success.

Understanding the strategic considerations in real estate syndication involves a keen focus on past performance, a critical element that shapes investor confidence. The expertise of the syndication team and property managers, especially in dealing with multifamily properties and commercial real estate assets, adds another layer to the strategic planning of an investment deal.

In the world of real estate syndication, where high returns are pursued, the choice of structures, such as limited liability companies, becomes crucial. Balancing a passive role for investors in the best way possible becomes one of the most important things in syndication. Factors like preferred return structures, investment portfolios, capital investment, and investment decisions contribute to creating a holistic strategy that aligns with the goals of both GPs and investors.

At Bridgestone Capital, we emphasize the strategic importance of ownership and compensation structures, creating a solid foundation for successful real estate syndication.

[divi_switch_layout id=”1311″]

Contact Jeff Davis at Bridgestone Capital via jeff.davis@bridgestoneinvest.com for expert advice and start building a real estate portfolio that stands the test of time.

Gain insights on achieving financial independence while working your W2 subscribe!

To receive information about passive income ideas please contact me at jeff.davis@bridgestoneinvest.com. We have syndications going on throughout the year.

Always consult with a financial advisor, CPA, or CFP to make sure your financial plans align with your goals, risk tolerance and financial situation.

In the ever-evolving landscape of financial planning, individuals are increasingly exploring alternative avenues to fortify their retirement accounts. One notable strategy gaining traction is the incorporation of real estate investments within retirement portfolios. As the scope of financial planning widens, so does the importance of understanding the benefits and complexities associated with unconventional approaches, such as leveraging a self-directed IRA for real estate ventures.

Traditional retirement plans, including mutual funds and Roth IRA s, have long been the cornerstone of retirement savings. However, the emergence of self-directed options allows investors to wield greater control over their portfolios, steering towards the diversification offered by tangible assets like real estate. This shift in strategy enables individuals to harness the potential of real estate while enjoying the tax advantages intrinsic to a well-structured retirement plan.

In this exploration of the intersection between retirement planning and real estate, we delve into the possibilities and considerations surrounding the use of a self-directed IRA. By broadening the horizon beyond conventional investment avenues like individual retirement accounts and traditional IRAs, investors can unlock a realm of possibilities that extends to diverse assets, including precious metals and personal funds.

Join us on this journey as we navigate the intricate landscape of self-directed retirement accounts, shedding light on the benefits, pitfalls, and operational nuances associated with integrating real estate into your retirement strategy. As the financial terrain transforms, understanding the power of a self-directed approach becomes paramount for savvy real estate investors looking to optimize their retirement portfolios.

The landscape of retirement planning has evolved beyond the traditional realms of Roth IRAs, individual retirement accounts, and traditional IRAs. Investors are increasingly drawn to the potential of self-directed options, offering a broader spectrum of investment opportunities. One such avenue that has gained prominence is utilizing a self-directed IRA for real estate transactions.

Unlike conventional retirement accounts tethered to the stock market or financial institutions, a self-directed IRA provides individuals with the autonomy to diversify their portfolios into alternative investments, including real estate. This shift allows investors to explore the potential of tangible assets, such as rental properties, mortgage notes, and investment properties.

However, navigating the terrain of self-directed IRAs for real estate involves understanding key concepts and adhering to regulatory guidelines. An essential element in this journey is the role of an IRA custodian, a designated entity responsible for facilitating the self-directed IRA and ensuring compliance with regulations.

One notable advantage of utilizing a self-directed IRA for real estate lies in the ability to employ non-recourse loans. These loans are secured by the property itself, limiting the liability to the property’s value and shielding the remaining retirement funds from potential losses.

[divi_switch_layout id=”1311″]

Investors must be mindful of certain rules and restrictions to avoid running afoul of IRS regulations. For instance, transactions involving disqualified persons, such as family members, could result in severe penalties. The intricacies of self-directed IRAs also require a keen understanding of the prohibited practice of using the account for personal benefit.

When contemplating a real estate purchase within the framework of a self-directed IRA, investors should weigh the advantages of property ownership against the potential challenges. While the self-directed IRA offers the potential for tax-advantaged growth, investors must be diligent in adhering to guidelines surrounding real estate transactions within qualified retirement plans.

In the realm of self-directed IRAs, the potential for combining real estate and retirement planning is vast. However, a nuanced approach, understanding the roles of IRA custodians, comprehension of alternative investments, and adherence to regulatory guidelines are crucial for a successful integration of real estate into your retirement strategy.

Key Differences Between Self-Directed IRAs and Traditional Retirement Accounts

As individuals explore the expansive realm of retirement planning, the distinctions between various account types, such as Roth IRAs, individual retirement accounts (IRAs), and traditional IRAs, become pivotal. However, the advent of self-directed retirement accounts introduces a new dimension, offering investors a level of control and flexibility that sets it apart from traditional counterparts.

One significant contrast lies in the realm of investment options. While traditional IRAs are often tethered to more conventional assets, such as stocks and bonds, self-directed IRAs empower investors to delve into a broader spectrum of opportunities, including real estate transactions, investment properties, and a diverse array of alternative assets.

The concept of a “disqualified person” is another critical distinction. In the context of self-directed IRAs, this term encompasses certain individuals with whom transactions are prohibited, such as family members. Understanding and navigating these prohibitions are paramount to avoiding penalties and maintaining compliance with Internal Revenue Service (IRS) regulations.

One unique feature of self-directed IRAs is the ability to leverage non-recourse loans for real estate investments. This financing option, secured by the property itself, provides investors with the means to amplify their purchasing power while mitigating personal liability and preserving their IRA account.

[divi_switch_layout id=”1311″]

For those seeking more hands-on control, the option of “checkbook control” in a self-directed IRA (retirement account) allows the plan owner to make investment decisions without requiring approval from a plan administrator. This level of autonomy is particularly appealing to business owners and entrepreneurs who value the agility to act swiftly in response to market opportunities.

In contrast, traditional retirement accounts often involve more rigid structures and limited investment options. While SEP IRAs and simple IRAs cater to business owners and the self-employed, they may lack the expansive scope of self-directed alternatives, limiting the range of potential investments.

Moreover, the concept of “catch-up contributions” in self-directed retirement accounts provides an avenue for individuals aged 50 and older to contribute additional funds, enhancing their retirement savings. This feature further underscores the flexibility and adaptability offered by self-directed IRAs.

As individuals consider the intricacies of self-directed retirement accounts, conducting thorough due diligence becomes imperative. Understanding the roles of plan administrators, complying with IRS guidelines, and recognizing the key differences between various account types are crucial steps in maximizing the benefits of a self-directed approach to retirement planning.

Conclusion: Maximizing Real Estate Opportunities in Self-Directed IRAs

In the dynamic realm of self-directed IRAs and real estate, the fusion of innovative strategies reveals a wealth of potential for investors. As we wrap up this exploration, let’s consolidate the key insights, emphasizing the crucial role of self-directed retirement accounts in navigating the intricacies of real estate investment.

Self-directed IRAs, including the distinctive Roth Solo, extend an unprecedented level of control and diversification for investors eyeing real estate, particularly in the realm of commercial properties. This autonomy allows for the exploration of alternative avenues, such as private equity, fostering a landscape where self-directed investors, small business owners, and those with a keen interest in real estate can thrive.

A crucial aspect of real estate investment within self-directed IRAs is understanding the financial implications. Whether it’s managing property taxes, mitigating capital gains, or strategizing with a property manager, investors must grasp the tax benefits and transaction rules inherent in real estate investing within this account type.

The integration of a self-directed IRA with a bank account adds a layer of convenience for investors, providing them with total control over their retirement assets. This is particularly beneficial for self-directed solo and small business owners, granting them the flexibility to optimize their retirement portfolio according to their unique goals.

As the landscape of real estate investing within self-directed IRAs unfolds, it becomes imperative for investors to navigate the intricacies of contribution limits and understand the tax breaks afforded to them. Leveraging the advantages of a self-directed IRA demands a comprehensive understanding of the various account types and the tax implications for the retirement account holder.

For those contemplating real estate investments within self-directed IRAs, the utilization of a limited liability company (LLC) and strategic considerations surrounding personal use of properties are paramount. Understanding the nuances of a nonrecourse loan, collaborating with a real estate agent, and exploring property management options contribute to the overall success of such ventures.

In conclusion, the synergy between self-directed IRAs and real estate offers a pathway to diversification, tax efficiency, and total control for investors. Whether you’re a seasoned real estate investor or a small business owner, the tax benefits and potential for substantial returns underscore the transformative power of integrating real estate into your self-directed retirement account. As you embark on this journey, remember that your self-directed IRA allows you to shape your financial future while maximizing the benefits of real estate investment.

[divi_switch_layout id=”1311″]

Contact Jeff Davis at Bridgestone Capital via jeff.davis@bridgestoneinvest.com for expert advice and start building a real estate portfolio that stands the test of time.

Gain insights on achieving financial independence while working your W2 subscribe!

To receive information about passive income ideas please contact me at jeff.davis@bridgestoneinvest.com. We have syndications going on throughout the year.

Always consult with a financial advisor, CPA, or CFP to make sure your financial plans align with your goals, risk tolerance and financial situation.

RSS Error: WP HTTP Error: A valid URL was not provided.

When delving into the realm of real estate investments, non-accredited investors often encounter the challenge of limited access to certain lucrative opportunities typically reserved for those with a higher income or net worth. Accreditation, as defined by the Securities and Exchange Commission (SEC), establishes criteria that classify investors based on income or net worth requirements. This classification, while segregating investors into categories like “accredited” and “non-accredited,” might initially seem discouraging for new investors eager to explore real estate.

For many new members entering the world of real estate investments, the realization that some doors are closed due to accreditation criteria can be disheartening. However, this article aims to empower non-accredited investors by shedding light on alternative investment avenues. As a non-accredited investor, you are not restricted from engaging in diverse and rewarding real estate opportunities.

Key Concepts:

Non-Accredited Investors

If you’re not an accredited investor, your level of awareness and interest in real estate investments is commendable. Many new investors start their journey by exploring passive income and financial freedom without initially understanding the complexities of accreditation.

Investment Opportunities

Despite limitations imposed by accreditation status, non-accredited investors have various avenues to explore in the real estate market. These opportunities allow for active participation, providing a chance to build a diversified investment portfolio and create passive income streams.

Real estate syndication deals, often associated with sophisticated investors and hedge funds, can also be accessible to non-accredited investors through specific channels. This article will guide you through different types of investments within the real estate sector.

Passive Income and Financial Freedom

The ultimate goal for many investors, regardless of accreditation status, is to achieve passive income and financial freedom. Understanding the available investment options is crucial for individuals looking to secure their financial future.

The focus of this article is on long-term investment strategies that allow non-accredited investors to actively participate in the real estate market. These strategies offer a balance between risk and potential returns.

In the following sections, we will explore eight ways in which non-accredited investors can engage in real estate investments. From traditional rental properties to innovative strategies like the BRRRR method, each option offers unique benefits and considerations. As we navigate through these opportunities, remember that your journey towards financial independence is a continuous learning process, and this article serves as a valuable resource in your pursuit of real estate success.

8 Ways ANYONE Can Invest In Real Estate

1. Buy and Hold Rentals

Most people are familiar with how having rental property works. You buy a home and rent it out.

The greatest perk to these types of investments is that you’re in charge. You can choose to manage it all yourself or hire a property management firm.

It’s your choice when to buy and when to sell, and you get to decide on the renovations.

The alternate to this power though is the responsibility. Everything rests on your shoulders, and when things go wrong, that’s on you too. Clogged toilet at 3 AM? It’s YOU that has to answer that call!

This is one of the main reasons I chose to invest in the passive route. I didn’t want a second job.

Rental properties are definitely open to the non-accredited investor, require a moderate level of work, and are long-term investments with a low-to-moderate risk.

Don’t Miss Any Updates. Each week I’ll send you advice on how to reach financial independence with passive income from real estate.

2. Fix and Flips

If you’re the type of investor that likes to take a hands-on approach, then fix and flips may be just the thing you need to get started.

These investments are usually a short-term purchase where you repair and remodel the property yourself and “flip” it (sell it for a profit).

The downside is that it might take substantial capital to get started, especially if you’re in an expensive area. This may be tough for the new doctor as they usually carry a boatload of student loan debt.

The cost to purchase the property, plus the value to fund the rehab, plus money to cover the mortgage payment until the property sells should all be set aside prior to making the deal.

You also face immediate market volatility and may have to hold the property longer than expected or sell for less than expected, which would cut into your potential profit.

It’s for these reasons that fix and flips typically carry a higher risk than some other options on this list.

The BRRRR strategy is a combination of the buy-and-hold and the fix-and-flip options.

It stands for:

Buy

Rehab

Rent

Refinance

Repeat

First Half:The first half of the strategy looks just like a fix-and-flip. You buy a property that needs some TLC and give the place a facelift.

Second Half:The second half of the strategy looks much more like a buy-and-hold. Once renovations are complete, you find tenants. Once rented, you do a cash-out refinance and repeat the process with another property.

Assuming after renovations were complete, the property’s value increased substantially, you may be able to pull out all of your original capital.

The BRRRR strategy is extremely powerful, open to a non-accredited investor, requires a high level of work, and is a long-term investment option with moderate-to-high risk.

One side of real estate investing that can easily be overlooked is investing in debt.

For example, this is where you loan someone money to complete a fix-and-flip.

You don’t have to be hands-on in the home purchase, renovations, or home selling process, nor do you have to be an accredited investor.

Most beginner investors are still working full time. Combine that lack of time (but a surplus of money) with a cash-strapped go-getter ready to do all the dirty work, and you have a deal.

As an example, you could loan them the fix-and-flip money for 12 months at 10% interest. They turn the house around within the 12-month period, and you earn 10% on the loan.

Your risk is relatively low because it’s backed by the property, your workload is low, and you don’t have to be accredited for these short-term investments.

8 Ways ANYONE Can Invest In Real Estate (Continued)

5. Joint Venture Partnerships

If single-family homes spell B-O-R-I-N-G to you, multifamily or commercial real estate might pique your interest.

If you also have the capital plus skills to contribute, you might be a great potential joint venture (JV) partner.

A JV partnership is where a small group invests together, and the property renovations and management tasks are split up between them.

Each person has an active role with no passive investors.

This type of opportunity is open to a non-accredited investor, has a high level of work, a moderate level of risk, and a flexible timeline depending on the project.

6. Real Estate Crowdfunding Platforms

Real estate crowdfunding platforms are much like Kickstarter, but for real estate. These platforms contain opportunities for a variety of projects from fix-and-flips to large-scale value-add multifamily projects.

You invest capital in exchange for a portion of the returns without having to do any of the work. Most of these types of opportunities are for accredited investors only.

However, there are a few real estate crowdfunding sites that offer REITs (real estate investment trusts) for non-accredited investors.

REITs don’t give you the benefits of direct ownership, but they are great vehicles for passive investing and typically require low minimum investments with low risk and a low threshold of work involved.

7. Private Real Estate Syndications

Group investments where people pool their resources to invest in a large asset is a real estate syndication deal. At first glance, this may sound a lot like a joint venture situation.

However, JV investors each have a specific, active role in managing the property. In a real estate syndication, most of the investors are passive – meaning they won’t be hands-on with the property renovations or making any big decisions.

This is the MAIN reason I almost exclusively invest in these types of investments in the real estate category.

Many real estate syndications are only open to accredited investors, due to SEC regulations. However, there are a wide variety of opportunities open to non-accredited investors as well.

Since the opportunities for non-accredited investors aren’t able to be publicly advertised, you have to know someone who’s part of a general partnership to gain access.

These deals require a low level of work (research and connection upfront) and carry low risk as a long-term investment.

Don’t Miss Any Updates. Each week I’ll send you advice on how to reach financial independence with passive income from real estate.

If you’re a new or passive investor, navigating the intricate landscape of real estate can be daunting. However, understanding the diverse opportunities available to you is crucial in your journey towards financial independence. Let’s distill some key takeaways from the eight ways anyone can invest in real estate.

Embrace Learning: For new investors, the learning curve can seem steep, but your commitment to understanding real estate investments is commendable. Continuously educate yourself to expedite your path to building passive income.

The Power of 8: The highlighted eight ways provide a spectrum of investment options. Each avenue caters to different preferences, risk appetites, and levels of involvement. New investors can explore these choices and tailor their strategies accordingly.

Active vs. Passive: Recognize the distinction between active and passive roles in real estate. Whether you choose to actively manage rental properties or passively invest in syndications, align your choices with your goals and preferences.

Diversification is Key: Real estate offers various investment vehicles, from traditional rentals to innovative crowdfunding platforms. Diversifying your real estate portfolio can mitigate risks and optimize returns over the long term.

Network and Collaborate: Opportunities like joint venture partnerships and private real estate syndications may require networking. Connect with experienced individuals, join investment circles, and leverage relationships to access deals that align with your goals.

Due Diligence Matters: Regardless of your experience level, conducting thorough due diligence is paramount. Evaluate potential real estate deals meticulously, seek advice from financial advisors, and take charge of your investment decisions.

Unlock Passive Income: The ultimate goal for many investors, both new and seasoned, is to achieve passive income. Real estate offers avenues for creating sustainable passive income streams, allowing you to live life on your terms.

Strategic Guidance: Engage with investment advisors and financial professionals who specialize in real estate. Their expertise can provide valuable insights and help you navigate the intricacies of the real estate market.

In essence, the eight ways highlighted in this article offer a roadmap for new and passive investors to embark on their real estate journey. As you explore these opportunities, remember that every investment decision should align with your financial goals and risk tolerance. Stay committed to your path, leverage the power of knowledge, and unlock the vast potential of real estate as a vehicle for financial growth.

Don’t Miss Any Updates. Each week, I’ll send you advice on how to reach financial independence with passive income from real estate.

Next up, we’ll delve into Bridgestone Capital and its role in multifamily syndications and joint ventures.

Bridgestone Capital – Navigating Multifamily Syndications and Joint Ventures

Bridgestone Capital: Your Partner in Real Estate Success